Most conversations about financial independence start with a number.

“How much do I need to retire?”

“What’s your FIRE (Financial Independence, Retire Early) number?”

“Is $1 million enough?”

These questions are understandable—but they’re incomplete.

They assume that financial independence is something you reach, like a finish line. That once your net worth crosses a certain threshold, freedom automatically follows.

In reality, financial independence works very differently.

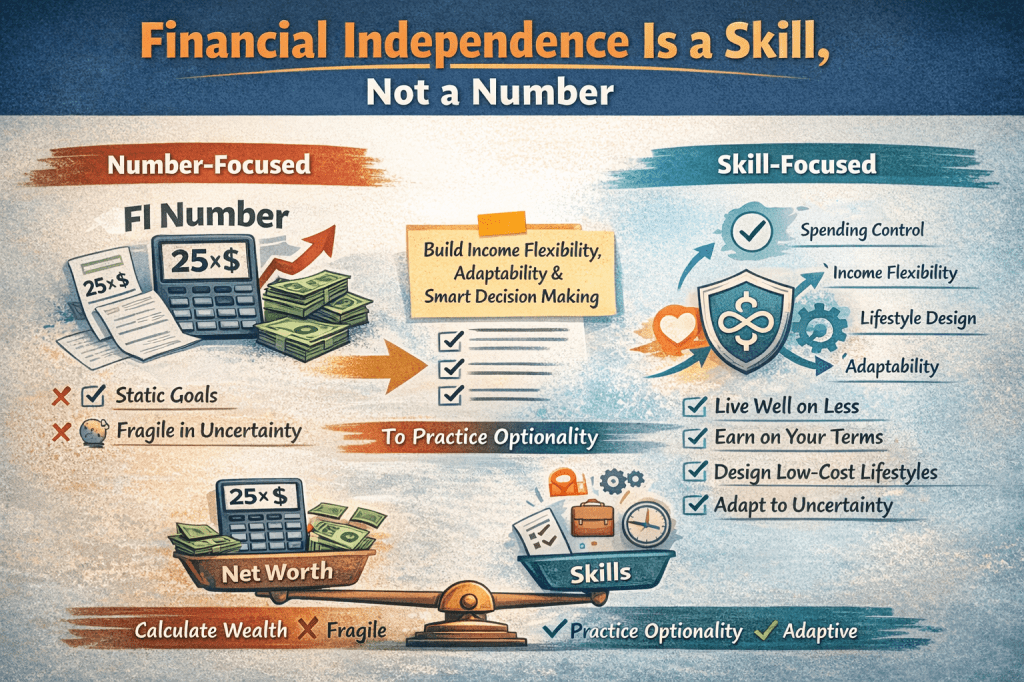

Financial independence is not a number.

It’s a skill.

And like any skill, it can be developed, refined, and adapted—or neglected and lost.

The illusion of the “FI number”

The FIRE movement popularized a simple framework:

- Estimate your annual spending

- Multiply it by 25

- Reach that number, and you’re “financially independent”

As a rough planning tool, this is useful. As a mental model for freedom, it’s dangerous.

Why?

Because it creates the illusion that:

- freedom is static

- life is predictable

- behavior doesn’t matter once the math works

None of these are true.

Markets change.

Health changes.

Goals change.

Costs change.

A number calculated at 35 doesn’t guarantee freedom at 55 if the underlying skills aren’t there.

What financial independence actually buys you

At its core, financial independence isn’t about stopping work.

It’s about reducing fragility.

It buys you:

- time flexibility

- decision flexibility

- income flexibility

- geographic flexibility

These aren’t outcomes of a net worth figure alone.

They’re outcomes of how you earn, spend, adapt, and decide.

That’s why two people with the same net worth can experience completely different levels of freedom.

Why skills beat numbers

A number is static.

A skill is adaptive.

Skills respond to change. Numbers don’t.

If inflation spikes, a skillful spender adjusts.

If income drops, a skillful earner pivots.

If markets fall, a skillful planner adapts withdrawals and expectations.

Without these skills, a “safe” number becomes fragile.

The core skills behind real financial independence

1. Spending control (without deprivation)

The most foundational FIRE skill isn’t investing.

It’s spending control.

Not extreme frugality.

Not deprivation.

But intentional spending aligned with values.

This skill allows you to:

- live well on less

- avoid lifestyle inflation

- scale spending up or down without stress

People who master this skill don’t fear downturns. They have margin.

Those who don’t remain anxious—even at high net worths.

2. Income flexibility

Traditional FIRE thinking treats income as binary:

- working vs retired

In reality, income exists on a spectrum.

Financial independence improves dramatically when you can:

- reduce hours

- change roles

- switch industries

- earn location-independent income

- monetize skills episodically

Someone who can reliably earn some income has far more freedom than someone with a larger portfolio but zero flexibility.

Income optionality is a skill.

3. Lifestyle design

Financial independence isn’t about affording everything.

It’s about designing a life that doesn’t cost much to maintain.

This includes:

- choosing locations intentionally

- avoiding status-driven expenses

- building low-cost, high-satisfaction routines

- optimizing for recurring happiness, not one-time splurges

People who ignore lifestyle design end up chasing ever-larger numbers.

People who master it lower the bar for independence every year.

4. Decision-making under uncertainty

Markets don’t move in straight lines. Neither do careers or lives.

Financial independence requires the ability to:

- make decisions without perfect information

- avoid panic during downturns

- resist lifestyle inflation during booms

- accept trade-offs consciously

This is not a math problem.

It’s a behavioral one.

The better your decision-making skill, the less you need a “buffer number” to feel safe.

5. Adaptability

The most underrated FIRE skill is adaptability.

Over a multi-decade timeline:

- industries disappear

- tax rules change

- personal priorities shift

- health becomes more valuable than money

People who treat FIRE as a fixed plan struggle when reality diverges.

People who treat it as an evolving system stay free.

Why number-based FIRE creates anxiety

Ironically, number obsession often increases stress instead of reducing it.

Common patterns:

- constantly recalculating the FIRE number

- feeling behind despite progress

- delaying life until “after FI”

- tying self-worth to net worth milestones

This happens because the number becomes an identity anchor.

When freedom is framed as a future state, the present always feels insufficient.

Skill-based FIRE flips this dynamic.

Skill-based FIRE starts paying off immediately

Unlike a distant number, skills compound in real time.

- Spending skill reduces stress this month

- Income flexibility creates confidence this year

- Lifestyle design improves daily quality of life

- Decision skill prevents costly mistakes

Freedom becomes a gradient, not a switch.

You don’t wake up one day “free.”

You feel increasingly less constrained.

Two FIRE paths, same net worth

Imagine two people with identical portfolios.

Person A

- High fixed expenses

- Specialized career

- No desire to earn again

- Lives in a high-cost area

- Needs everything to go right

Person B

- Low, flexible expenses

- Broad skill set

- Comfortable earning occasionally

- Geographically flexible

- Comfortable adapting plans

Same number.

Completely different freedom.

The difference isn’t money.

It’s skill.

Rethinking the FIRE question

Instead of asking:

“What’s my financial independence number?”

Try asking:

- How adaptable is my lifestyle?

- How flexible is my income?

- How quickly can I reduce expenses if needed?

- How confident am I navigating uncertainty?

- How dependent am I on everything going according to plan?

These answers matter more than any spreadsheet.

The compounding effect of FIRE skills

The beauty of skill-based financial independence is that it compounds outside markets.

- Better spending habits reduce required savings

- Lower savings targets reduce burnout

- Less burnout increases career longevity

- More longevity improves income optionality

This feedback loop is why many people reach FIRE “by accident” after focusing on skills instead of numbers.

When the number still matters

None of this means the math is irrelevant.

You still need:

- sufficient assets

- reasonable withdrawal assumptions

- risk awareness

- margin of safety

But the number should be:

- a guideline, not an idol

- a tool, not an identity

- flexible, not sacred

Skills give the number context.

Financial independence as antifragility

The strongest form of FIRE isn’t optimized for perfect conditions.

It’s optimized for:

- uncertainty

- volatility

- change

This is why skill-based FIRE feels calmer.

You’re not betting everything on:

- one market outcome

- one career

- one lifestyle

- one assumption

You’re building antifragility.

A practical reframing

If you want a simpler mental model, try this:

Financial independence is the ability to maintain a good life across a wide range of scenarios.

That ability is learned.

Final takeaway

Numbers matter—but they don’t protect you.

Skills do.

If you focus only on the size of your portfolio, financial independence will always feel fragile and distant.

If you build the skills of spending control, income flexibility, lifestyle design, and adaptability, freedom arrives earlier—and lasts longer.

Because in the end, financial independence isn’t something you reach.

It’s something you practice.

Leave a comment