In investing, expense ratios matter.

A fund that quietly charges 1% per year doesn’t look dangerous. But over decades, that small drag compounds into a massive difference in outcomes.

Life works the same way.

Every frugal choice carries an expense ratio—not just in money, but in time, energy, health, and optionality. Some frugal decisions quietly compound in your favor. Others create hidden costs that erode the very freedom you’re trying to buy.

The mistake isn’t frugality itself.

It’s being frugal in the wrong places.

This article is about learning where frugality compounds—and where it backfires.

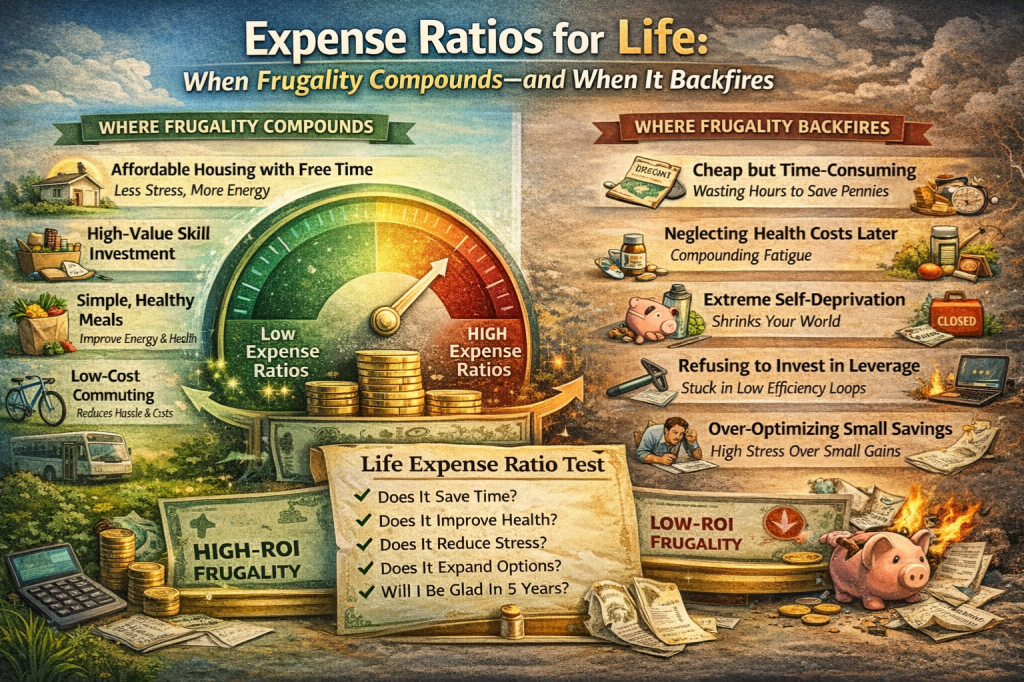

Frugality isn’t Binary. It’s Directional.

Most personal finance advice treats frugality as a virtue in itself.

Spend less.

Save more.

Repeat.

That framing is incomplete.

Frugality isn’t good or bad. It’s directional. It either:

- Expands your future options, or

- Shrinks your life to protect a number

The difference lies in the secondary effects—what a decision enables or disables over time.

That’s your real expense ratio.

The Life Expense Ratio Framework

Think of every recurring decision as having an ongoing “fee” attached to it.

Not a financial fee—but a cost in:

- Time

- Energy

- Health

- Stress

- Opportunity

- Optionality

Low life expense ratios free resources to compound elsewhere.

High life expense ratios quietly tax your future.

Money is only one variable.

Where Frugality Compounds

Some frugal choices are pure leverage. They lower costs and improve life.

These are the decisions worth defending aggressively.

1. Housing That Buys Time, Not Status

Housing is usually the largest recurring expense—and the biggest opportunity for compounding frugality.

High-ROI frugality looks like:

- Living slightly below what you can afford

- Optimizing for location efficiency, not square footage

- Reducing commute time and friction

The real return isn’t lower rent—it’s:

- More time

- Less stress

- More energy for work, health, and relationships

A cheaper home that costs you hours of commuting has a terrible life expense ratio.

2. Transportation That Reduces Cognitive Load

Cars are often framed as financial drains, but the real cost is mental overhead.

High-ROI frugality here means:

- Owning fewer vehicles

- Choosing reliability over prestige

- Designing life around walking, biking, or simple transport

Every avoided breakdown, traffic jam, and maintenance hassle compounds into reclaimed attention.

Frugal transportation decisions often double as health investments.

3. Food Systems That Reduce Decision Fatigue

Cheap food isn’t always frugal.

Low-ROI frugality looks like:

- Buying the cheapest options that damage energy and health

- Constantly optimizing grocery prices without a system

High-ROI frugality looks like:

- Simple, repeatable meals

- Fewer decisions

- Buying quality where it reduces friction

A slightly higher grocery bill that saves time, improves energy, and stabilizes health compounds positively.

4. Recurring Subscriptions You Actually Use

The mistake isn’t subscriptions—it’s unused subscriptions.

High-ROI frugality:

- Ruthlessly cuts unused recurring costs

- Keeps high-value tools that save time or improve output

A $20 tool that saves you an hour a week has an extraordinary return.

Expense ratios rise when you pay repeatedly without receiving value.

5. Skill-Building Over Consumption

Frugality compounds when it shifts spending from consumption to capability.

Examples:

- Buying fewer things, but better tools

- Investing in skills that reduce future costs

- Learning to cook, fix, write, or negotiate

Skills lower future expense ratios across many domains.

They are one-time investments with lifelong returns.

Where Frugality Backfires

Some frugal decisions look smart on a spreadsheet—but quietly sabotage progress.

These are the traps that delay FIRE and degrade life quality.

1. Being Cheap With Health

Health neglect is the most expensive form of frugality.

Skipping:

- Movement

- Sleep

- Recovery

- Preventative care

…doesn’t save money. It defers costs with interest.

Low-ROI frugality shows up as:

- Chronic fatigue

- Reduced productivity

- Limited mobility

- Medical expenses later

Health has the highest compounding curve of any asset you own.

2. Time-Expensive Savings

If a frugal action costs you hours to save a few dollars, it’s usually a bad trade.

Examples:

- Driving far for minor discounts

- Over-optimizing small purchases

- Constantly comparison shopping low-impact items

Time is a non-renewable asset.

High life expense ratios often hide behind “saving money.”

3. Frugality That Increases Stress

Some people win the savings game and lose the psychological one.

Signs frugality is backfiring:

- Constant anxiety around spending

- Guilt over reasonable purchases

- Fear of lifestyle creep that blocks growth

Frugality should reduce stress, not create it.

If saving money dominates mental bandwidth, the expense ratio is too high.

4. Under-Investing in Leverage

Extreme frugality often avoids spending on anything that isn’t “necessary.”

That includes:

- Tools

- Education

- Systems

- Delegation

Avoiding these can trap you in low-leverage loops.

A cheap laptop that slows work, or refusing help that frees time, quietly taxes your earning potential.

5. Frugality That Shrinks Your World

The most dangerous form of frugality is self-contraction.

It looks like:

- Avoiding experiences entirely

- Saying no by default

- Designing life around deprivation

This doesn’t build freedom—it builds resentment.

FIRE achieved through misery isn’t independence. It’s endurance.

Frugality vs Optimization: A Useful Distinction

Frugality asks: How can I spend less?

Optimization asks: How can I get better outcomes?

The best decisions do both—but if forced to choose, optimization usually wins.

You don’t need the cheapest option.

You need the lowest total cost over time.

A Simple Test for Frugal Decisions

Before cutting or adding an expense, ask:

- Does this save money and time?

- Does this improve or degrade health?

- Does this increase or reduce stress?

- Does this expand future options?

- Will I still be glad I did this in 5 years?

If most answers are positive, frugality compounds.

If not, it backfires.

Frugality as Risk Management

The best role of frugality isn’t austerity—it’s risk reduction.

High-ROI frugality:

- Lowers fixed costs

- Increases flexibility

- Buys resilience

This is why frugality pairs so well with FIRE (Financial Independence, Retire Early).

Not to escape life—but to design one that absorbs shocks.

The Long Game

Frugality is a tool, not a value system.

Used well, it accelerates freedom.

Used blindly, it delays it.

The goal isn’t to minimize spending.

It’s to minimize life expense ratios.

Spend aggressively where returns compound.

Cut ruthlessly where costs quietly accumulate.

That’s how frugality stops being restrictive—and starts becoming powerful.

Leave a comment