Not all paths to financial independence look the same. Here’s how to find the one that actually fits your life — not someone else’s spreadsheet.

Financial independence doesn’t have a single definition. For some, it means never working another day. For others, it means working on their own terms — a few shifts a week, a passion project, a small business that covers the basics while their portfolio quietly compounds in the background.

The FIRE movement (Financial Independence, Retire Early) has evolved far beyond its original “save aggressively, retire at 35” narrative. Today, there are multiple paths — each with different assumptions about spending, risk, lifestyle, and what “enough” actually means.

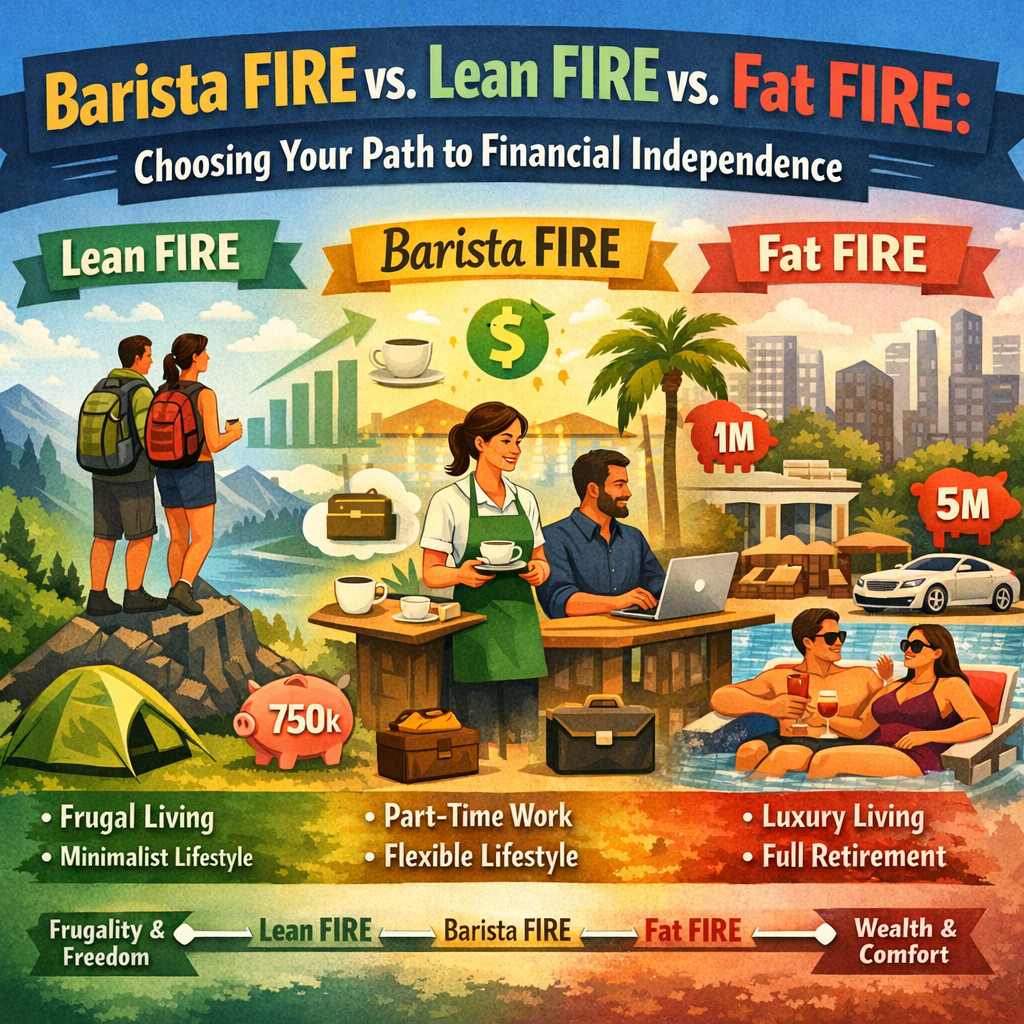

The three most talked-about variations are Lean FIRE, Barista FIRE, and Fat FIRE. They sit on a spectrum, and understanding where you fall isn’t just a financial question — it’s a lifestyle design question.

Let’s break down each one, compare them honestly, and help you figure out which path actually fits your life.

What Is Lean FIRE?

Lean FIRE is the minimalist’s path to financial independence. The idea is simple: keep your annual expenses low — typically under $40,000 per year for an individual — and build a portfolio that sustains that level of spending indefinitely.

If you follow the traditional 4% rule, that means you’d need roughly $750,000 to $1,000,000 saved to consider yourself financially independent under a Lean FIRE framework.

The philosophy behind Lean FIRE:

- You don’t need a high income to reach financial independence — you need low expenses

- Frugality isn’t a phase; it’s a permanent lifestyle choice

- Freedom matters more than comfort, and simplicity is the vehicle

Who Lean FIRE works for:

- People who genuinely enjoy a minimalist lifestyle — not those forcing themselves into one

- Those who live in low cost-of-living areas or practice geoarbitrage

- Individuals or couples without significant healthcare costs, debt obligations, or dependents

- People who find meaning in simplicity and don’t feel deprived by spending less

The trade-offs:

Lean FIRE offers the fastest path to independence, but it comes with the thinnest margin of safety. One unexpected expense — a medical bill, a major repair, a family emergency — can throw your plan off balance. There’s also the psychological cost. If your budget is perpetually tight, the freedom you worked so hard to achieve can start to feel like a different kind of constraint.

Lean FIRE works beautifully when it’s authentic. It breaks down when it’s performative — when you’re cutting expenses not because you want less, but because you’re racing toward a number.

What Is Barista FIRE?

Barista FIRE sits in the middle of the spectrum and is arguably the most practical path for most people. The name comes from the idea that you could work a low-stress, part-time job — like a barista at a coffee shop — to cover your basic living expenses while your investment portfolio continues to grow untouched.

You’re not fully financially independent yet. But you’ve saved enough that you no longer need a high-paying, high-stress career to survive. You’ve bought yourself optionality.

The philosophy behind Barista FIRE:

- You don’t have to wait until you’re 100% financially independent to reclaim your time

- A small amount of earned income dramatically reduces the pressure on your portfolio

- Work becomes a choice, not an obligation — and that changes everything

Who Barista FIRE works for:

- People who want to leave demanding careers but aren’t ready (or willing) to stop earning entirely

- Those who enjoy some form of work — freelancing, consulting, teaching, part-time roles — but want it on their own terms

- People who want benefits like health insurance through an employer (especially relevant in the US)

- Digital nomads, creatives, and lifestyle designers who earn variable income

The math:

Let’s say your annual expenses are $50,000. If you earn $20,000 per year from part-time or freelance work, your portfolio only needs to cover $30,000. Using the 4% rule, that’s a required portfolio of roughly $750,000 instead of $1,250,000. That difference could mean reaching your version of independence 5 to 10 years sooner.

The trade-offs:

Barista FIRE requires you to keep earning some income — and that means it’s not full independence. If your part-time income disappears or your health prevents you from working, you’re back to relying entirely on your portfolio, which may not be large enough yet. It also requires a mindset shift: you have to be comfortable with “enough” rather than “completely done.”

But for most people, Barista FIRE is where freedom begins — not at the finish line, but somewhere in the middle.

What Is Fat FIRE?

Fat FIRE is financial independence without compromise. The goal is to accumulate a large enough portfolio that you can maintain a comfortable, even luxurious lifestyle without ever needing to work again. Annual spending targets typically range from $100,000 to $200,000+, which means portfolio targets of $2.5 million to $5 million or more.

The philosophy behind Fat FIRE:

- Financial independence shouldn’t require sacrificing the lifestyle you enjoy

- You’ve earned the right to live well — and your portfolio should reflect that

- Freedom means never having to think about money again, not just covering the basics

Who Fat FIRE works for:

- High earners — tech professionals, doctors, lawyers, entrepreneurs, senior executives

- People who enjoy premium experiences and don’t want to downgrade their lifestyle

- Those with families, dependents, or complex financial obligations

- People in high cost-of-living cities who don’t plan to relocate

The trade-offs:

The obvious one: time. Fat FIRE takes significantly longer to achieve. If you’re saving aggressively on a $200,000 salary, you might still be looking at 15 to 20 years before your portfolio can sustain $150,000 in annual spending. During that time, you’re often locked into high-pressure, high-income careers — the very thing you’re trying to escape.

There’s also a subtle psychological trap. The lifestyle that demands Fat FIRE-level spending is often the same lifestyle that makes you feel like you need to keep earning. Lifestyle inflation doesn’t just slow your savings rate — it moves the finish line further away.

Fat FIRE works when your high income is sustainable and your spending is intentional. It stalls when spending grows reflexively and the goalpost keeps shifting.

A Side-by-Side Comparison

| Factor | Lean FIRE | Barista FIRE | Fat FIRE |

|---|---|---|---|

| Annual Spending | Under $40K | $40K–$60K | $100K–$200K+ |

| Portfolio Target | $750K–$1M | $750K–$1.25M | $2.5M–$5M+ |

| Income After FIRE | None | Part-time/freelance | None |

| Time to Achieve | Fastest | Moderate | Longest |

| Lifestyle Flexibility | Low | Moderate | High |

| Margin of Safety | Thin | Moderate (with income) | Wide |

| Risk Tolerance Required | High | Moderate | Low |

| Best For | Minimalists | Lifestyle designers | High earners |

How to Choose the Right Path

Here’s the truth most FIRE content won’t tell you: you don’t have to pick one and stick with it forever.

Your FIRE path isn’t a permanent identity. It’s a strategy — and strategies should evolve as your life does. Many people start with Lean FIRE as a target, realize Barista FIRE gives them enough freedom to stop grinding, and eventually drift toward Fat FIRE as their career or investments grow.

Instead of asking “Which FIRE type am I?”, ask yourself these five questions:

1. What does your ideal Tuesday look like?

Not your dream vacation — your average day. If it’s simple and low-cost, Lean FIRE might be your natural fit. If it includes some form of meaningful work, Barista FIRE aligns well. If it involves a level of comfort that requires significant spending, you’re looking at Fat FIRE.

2. How do you feel about continued work?

If the idea of never working again is the whole point, you need full financial independence (Lean or Fat). If you enjoy working but hate being forced to, Barista FIRE gives you the best of both worlds.

3. What’s your actual annual spending — not your ideal one?

Track it honestly for three to six months. Most people underestimate their spending when planning for Lean FIRE and overestimate what they need for Fat FIRE. Your real number determines your real target.

4. How important is a margin of safety to you?

If market downturns or unexpected expenses would keep you up at night, a thinner portfolio (Lean FIRE) might create more anxiety than freedom. Barista FIRE’s earned income buffer or Fat FIRE’s larger cushion might suit your temperament better.

5. Where do you plan to live?

Geography changes everything. $40,000 a year is abundant in Chiang Mai or Medellín. It’s barely survival in San Francisco or London. Your FIRE type is inseparable from your location strategy.

The Path Most People Miss

The most sustainable version of financial independence usually isn’t the most extreme one. It’s the version where your spending reflects your real values, your savings rate is high but not punishing, and your relationship with work shifts from obligation to choice.

For most people reading this, Barista FIRE is the most underrated and overlooked path. It doesn’t get the flashy headlines. It doesn’t have the dramatic “I retired at 32” story. But it offers something more valuable — a life you don’t need to escape from, funded by a portfolio you don’t need to panic about.

Financial independence isn’t a single destination. It’s a spectrum. The goal isn’t to reach the most impressive number — it’s to reach the number that gives you back your time, your energy, and your choices.

Start there. The rest compounds on its own.

Related Reading

If this post resonated with you, here are some related posts from the blog that go deeper into the ideas mentioned above:

- The Boring Middle of FIRE: How to Stay Consistent While Compounding Works

- Why Financial Independence Is Really About Slack (Not Early Retirement)

- Coast FIRE Explained: The Ultimate Lifestyle Upgrade for People Who Don’t Hate Their Jobs

- Designing Cash Flow for Financial Independence (Not Maximum Returns)

- The First $100K Is the Hardest: Why Reaching $100,000 Changes Your Financial Freedom

- How to Reduce Financial Stress Without Earning More (The Lifestyle Beta Approach)

- The Second-Order Effects of Frugality: When Saving Money Starts to Cost You

- Expense Ratios for Life: When Frugality Compounds — and When It Backfires

- Financial Independence Without Extremes: A Sustainable Approach to FIRE

- Time vs Money: Which One Compounds Faster for Long-Term Freedom?

- Why FIRE Isn’t Sustainable Without Financial Slack

- Geoarbitrage 101: Living Well for Less Around the World

- The Optionality Playbook: Why Financial Independence Is About Better Choices, Not Early Retirement

- Financial Independence Is a Skill, Not a Number

Leave a comment