The 4% rule has become gospel in the FIRE (Financial Independence, Retire Early) community. Withdraw 4% of your portfolio in year one, adjust for inflation annually, and your money should last 30 years. It’s simple, reassuring, and backed by historical data.

But here’s what most people miss: the 4% rule was designed for traditional 30-year retirements starting at age 65. If you retire at 35 or 40, you’re looking at a 50+ year time horizon. The math changes dramatically.

Even more counterintuitively, spending more in the early years of financial independence—when your portfolio returns are strong—might actually be safer than rigidly sticking to 4%. This isn’t permission for reckless spending. It’s about understanding dynamic withdrawal strategies that adapt to market performance rather than following a fixed percentage into potential disaster.

Let me explain why flexibility beats rigidity, and how to implement a dynamic withdrawal approach that maximizes your quality of life without running out of money.

The Fatal Flaw in the 4% Rule

The 4% rule assumes you’ll withdraw the same inflation-adjusted amount every single year, regardless of market performance. Retire with $1 million? You withdraw $40,000 in year one, then adjust that $40,000 for inflation annually—even if the market crashes 40% the next year.

This creates two problems:

Problem 1: Sequence of returns risk

If you experience poor market returns in the first 5-10 years of retirement, you’re selling assets at depressed prices to maintain your spending. This locks in losses and dramatically increases the chance of portfolio depletion.

The 4% rule’s solution? Be conservative enough to survive the worst-case scenarios. But this means underspending in most scenarios.

Problem 2: Lifestyle rigidity

Your health, energy, and interests change over time. Spending the same inflation-adjusted amount at 40 as you do at 70 doesn’t match reality. You’ll likely want to travel more, try new things, and be physically active in your early retirement years. By 70, healthcare might increase, but your desire to backpack Southeast Asia probably won’t.

The 4% rule ignores the fact that retirement isn’t linear—it’s a series of distinct phases with different spending patterns and needs.

What Dynamic Withdrawal Rates Actually Mean

Dynamic withdrawal strategies adjust your spending based on portfolio performance and other factors. Instead of committing to a fixed dollar amount, you recalculate your withdrawal percentage annually (or use guardrails) based on current portfolio value.

The key insight: your spending should flex with your portfolio, not against it.

When markets perform well, you can afford to spend more. When markets decline, you trim temporarily. This approach dramatically reduces the risk of depleting your portfolio because you’re never forcing yourself to sell assets at the worst possible time.

Think of it like driving. The 4% rule is cruise control—you set a speed and maintain it regardless of road conditions. Dynamic strategies are adaptive cruise control—you maintain general direction but adjust to terrain, traffic, and weather.

Why Spending More Early Can Be Safer

Here’s the paradox: if your portfolio performs well in the early years of FIRE, spending more during that period can actually reduce long-term risk.

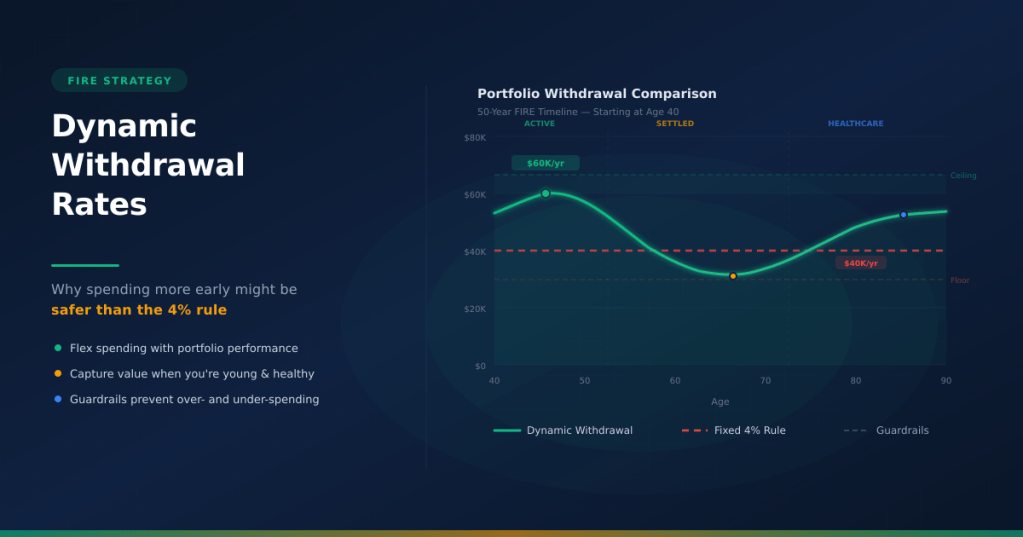

The “smile pattern” of retirement spending

Research shows that real retirement spending typically follows a smile curve:

- Early years (40-55): Higher spending on travel, experiences, active pursuits

- Middle years (55-70): Lower spending as lifestyle settles

- Later years (70+): Increased spending on healthcare and assistance

The 4% rule forces you to smooth this curve artificially. But life doesn’t work that way.

When front-loading spending makes mathematical sense

Imagine you retire with $1 million, and the market delivers exceptional returns in years 1-5, growing your portfolio to $1.5 million despite your withdrawals.

Under the 4% rule, you’d still be withdrawing based on your original $1 million (adjusted for inflation)—say $42,000 in year five. But your portfolio has grown 50%. You’re being unnecessarily conservative.

A dynamic approach might allow you to withdraw 5% in year five ($75,000) because your portfolio can handle it. You enjoyed higher quality of life when you were younger and healthier, and your portfolio is still in excellent shape.

The optionality advantage

By spending more when markets are good, you build experiential capital early—memories, skills, relationships, and health that compound over time. You can’t go back and travel at 70 the way you could at 40.

Meanwhile, if markets perform poorly early, you simply cut back. The key is having the flexibility to adjust, which brings us to implementation.

How to Implement Dynamic Withdrawal Strategies

There are several proven approaches. You don’t need to pick just one—you can blend elements based on your risk tolerance and lifestyle.

1. The Percentage-Based Method

Instead of withdrawing a fixed dollar amount, withdraw a fixed percentage of your portfolio’s current value each year.

Example:

- Year 1: Portfolio = $1M, withdraw 4% = $40,000

- Year 2: Portfolio = $900K (market down), withdraw 4% = $36,000

- Year 3: Portfolio = $1.1M (market recovers), withdraw 4% = $44,000

Pros: Simple, automatically adjusts to market conditions, virtually eliminates sequence risk.

Cons: Income volatility can be jarring; requires lifestyle flexibility.

Best for: People with variable expenses, geographic flexibility, or part-time income.

2. Guardrails Method (Guyton-Klinger)

Set upper and lower spending guardrails around your initial 4% withdrawal.

Example:

- Start with 4% of $1M = $40,000

- Upper guardrail: If portfolio grows 20% above inflation-adjusted starting value, increase spending by 10%

- Lower guardrail: If portfolio drops 20% below inflation-adjusted starting value, decrease spending by 10%

Pros: Provides structure and predictability; still allows flexibility.

Cons: More complex to track; requires discipline to cut spending when guardrails are hit.

Best for: People who want structure but recognize the limits of fixed withdrawal rates.

3. The Ratcheting Method

Allow spending to increase when markets perform well, but never decrease it below the previous year’s level (inflation-adjusted).

Example:

- Year 1: $40,000

- Year 2: Market up 25%, increase to $45,000

- Year 3: Market down 20%, maintain $45,000 (inflation-adjusted)

- Year 4: Market recovers, increase to $48,000

Pros: Prevents lifestyle deflation; captures upside during good years.

Cons: Can still deplete portfolio if you experience prolonged poor returns after ratcheting up.

Best for: People who need income stability and won’t accept lifestyle decreases.

4. The Actuarial Method

Recalculate your withdrawal rate annually based on remaining life expectancy and portfolio value—similar to required minimum distributions (RMDs) but starting earlier.

Example:

- Age 40, $1M portfolio, 50-year time horizon: withdraw 2.5%

- Age 50, $1.2M portfolio, 40-year time horizon: withdraw 3.2%

- Age 60, $1.5M portfolio, 30-year time horizon: withdraw 4.2%

Pros: Most conservative; mathematically sound; spending automatically increases with age.

Cons: Very low spending in early years; requires long-term patience.

Best for: People with very long time horizons or conservative risk tolerance.

My Recommended Hybrid Approach

After years of modeling and observing real FIRE practitioners, I recommend a hybrid strategy that blends flexibility with guardrails:

Start with 3.5-4% of your portfolio, then:

- Recalculate annually based on current portfolio value (percentage method)

- Set a floor at 80% of your initial withdrawal (inflation-adjusted) to prevent lifestyle collapse

- Set a ceiling at 150% of your initial withdrawal to prevent overspending during boom years

- Review every 3-5 years and adjust guardrails based on age, health, and goals

Example in practice:

You retire at 40 with $1 million.

- Year 1: Withdraw 4% = $40,000

- Year 2: Portfolio grows to $1.1M. Withdraw 4% = $44,000 (within ceiling)

- Year 3: Market crashes, portfolio drops to $800K. Withdraw 4% = $32,000, but floor prevents going below $32,000 (80% of $40,000). You withdraw the floor amount.

- Year 4: Portfolio recovers to $950K. Withdraw 4% = $38,000

- Year 5: Portfolio at $1.3M. Withdraw 4% = $52,000, but ceiling caps you at $60,000 (150% of original). You withdraw $52,000.

This approach gives you upside when markets are good, protection when they’re bad, and prevents extreme lifestyle swings in either direction.

When to Spend More (and When to Pull Back)

Green light to increase spending:

- Your portfolio has grown 20%+ above your FIRE number (inflation-adjusted)

- You’re in your first decade of FIRE and have high-energy goals (travel, adventure, learning)

- You have side income or semi-retirement work that covers part of your expenses

- Major markets (US, international) are in multi-year bull runs

- Your withdrawal rate is below 3%

Yellow light—proceed with caution:

- Portfolio is within 10% of your FIRE number

- Markets are volatile but not clearly trending down

- You’re between ages 50-65 (transitional spending phase)

- Withdrawal rate is 3.5-4.5%

Red light—time to cut back:

- Portfolio has declined 20%+ from peak

- Withdrawal rate exceeds 5% for more than one year

- You’re experiencing sequence of returns risk (poor returns in first 5-10 years)

- Major unexpected expenses are coming (health issues, family support)

- You’re uncomfortable with current burn rate

The Psychological Component: Why This Is Harder Than It Sounds

Dynamic withdrawal strategies are mathematically superior to the 4% rule in most scenarios. So why doesn’t everyone use them?

Because variability is uncomfortable.

Humans prefer predictability. A fixed $40,000 per year feels safer than “$36,000-$50,000 depending on the market.” Even if the dynamic approach is objectively safer long-term, it feels riskier.

The solution isn’t to ignore this psychology—it’s to design around it:

Build in buffers:

- Keep 1-2 years of expenses in cash or short-term bonds

- Maintain geographic flexibility (if rent increases, move to a lower-cost city)

- Preserve the option for part-time work

- Build skills that could generate income if needed

Reframe spending cuts as temporary:

A 10% spending reduction during a bear market isn’t failure—it’s the system working as designed. You’re preserving your portfolio so you can spend more over the next 40 years.

Track your “safety margin”:

Instead of obsessing over portfolio value, track how far you are from danger. If your withdrawal rate is 3.2% and your floor is 5%, you have 1.8 percentage points of safety margin. That’s what matters.

The Real Question: What Do You Want to Optimize For?

The 4% rule optimizes for certainty of not running out of money.

Dynamic withdrawal strategies optimize for maximum quality of life across your entire retirement.

Neither is wrong. It depends on what you’re afraid of.

If your greatest fear is running out of money at 85, the 4% rule (or even 3.5%) makes sense. You’ll likely die with a huge portfolio, but you’ll sleep well at night.

If your greatest fear is being too cautious in your 40s and 50s—when you’re healthy and energetic—only to realize at 70 that you have $3 million and a body that can’t use it, dynamic strategies are better.

I’d argue most FIRE pursuers are already more conservative than they need to be. If you hit your FIRE number, you’ve demonstrated discipline, planning, and risk management. You’re not the person who needs to be warned about overspending.

You might be the person who needs permission to spend more strategically.

Practical Implementation Steps

Step 1: Calculate your current withdrawal rate (annual spending ÷ portfolio value)

Step 2: Set your floor and ceiling based on lifestyle flexibility

- High flexibility: 70-200% of baseline

- Moderate flexibility: 80-150% of baseline

- Low flexibility: 90-120% of baseline

Step 3: Choose your recalculation frequency (I recommend annually, at year-end)

Step 4: Build 12-24 months of cash reserves to buffer market volatility

Step 5: Create a “lifestyle adjustment menu”—specific things you’d cut if you hit your floor, and specific things you’d add if you hit your ceiling

Step 6: Review annually and adjust as needed

Final Thoughts

The 4% rule isn’t wrong—it’s just incomplete. It was designed for a specific scenario (30-year retirement starting at 65) and doesn’t account for the realities of early retirement, sequence risk, or the changing nature of spending across decades.

Dynamic withdrawal strategies aren’t about spending recklessly. They’re about building a system that adapts to reality rather than forcing reality to adapt to a rigid rule.

If your portfolio doubles in the first decade of FIRE, spending more isn’t indulgent—it’s rational. If markets crash, cutting back isn’t failure—it’s smart risk management.

The paradox is real: spending more when times are good can make your retirement safer because you’re not forcing yourself to sell in downturns, and you’re capturing the value of money when it matters most—when you’re young enough to use it.

Financial independence isn’t about dying with the most money. It’s about living the best life your resources allow, for as long as possible.

Dynamic withdrawal strategies help you do exactly that.

Related Reading

FIRE Strategy & Planning:

- The First $100K Is the Hardest: Why Reaching $100,000 Changes Your Financial Freedom

- Why Financial Independence Is Really About Slack (Not Early Retirement)

- The Optionality Playbook: Why Financial Independence Is About Better Choices, Not Early Retirement

- FIRE Math Made Simple: Breaking Down the 4% Rule

- The Boring Middle of FIRE: How to Stay Consistent While Compounding Works

- Why Your FIRE Progress Feels Slow (And What to Do About It)

- Financial Independence is a skill, not a number

Spending & Lifestyle Design:

- The Psychology of Enough: How to Redefine Wealth Beyond Money

- Why FIRE Isn’t Sustainable Without Financial Slack

- How to Reduce Financial Stress Without Earning More (The Lifestyle Beta Approach)

- The Second-Order Effects of Frugality: When Saving Money Starts to Cost You

- Expense ratios for life: When frugality compounds – and when it backfires

- Lifestyle Inflation Detox: How to Save More and Spend Smarter as You Earn More

FIRE Approaches & Variations:

- Barista FIRE vs. Lean FIRE vs. Fat FIRE Explained: How to Choose the Right Path to Financial Independence

- Coast FIRE Explained: The Ultimate Lifestyle Upgrade for People Who Don’t Hate Their Jobs

- Financial Independence Without Extremes: A Sustainable Approach to FIRE

- FIRE as a Lifestyle Upgrade, Not a Career Downgrade

Post-FIRE Life:

- Life After Financial Independence: How to Navigate the Identity Crisis When Work No Longer Defines You

- Time vs Money: Which One Compounds Faster for Long-Term Freedom?

Planning & Optimization:

- Designing Cash Flow for Financial Independence (Not Maximum Returns)

- Time Arbitrage: How Flexible Schedules Help You Save More, Spend Less, and Build Wealth

- Freedom Forecasting: How to Predict Your FIRE Date with a Simple Framework

- The 80/20 of FIRE: Tiny Financial Tweaks That Create Outsized Results (Fast)

Leave a comment