When I first discovered the FIRE (Financial Independence, Retire Early) movement, the math behind it seemed overwhelming. Spreadsheets, investment calculators, withdrawal rates—it felt like a secret code only financial wizards could crack.

Then I came across the 4% Rule, and suddenly things clicked. It’s not perfect, but it’s a simple way to understand how much you need to retire early—and it’s the foundation of many FIRE plans.

🔢 What Is the 4% Rule?

The 4% Rule comes from a famous study called the Trinity Study, which looked at how long retirement portfolios lasted under different withdrawal rates. The conclusion: if you withdraw 4% of your portfolio each year, your money has a high probability of lasting at least 30 years.

In plain English:

- If you have $1,000,000 invested, you can withdraw $40,000 per year (4%) and likely not run out of money.

- If you need $30,000 per year to live on, you’d aim for a portfolio of $750,000.

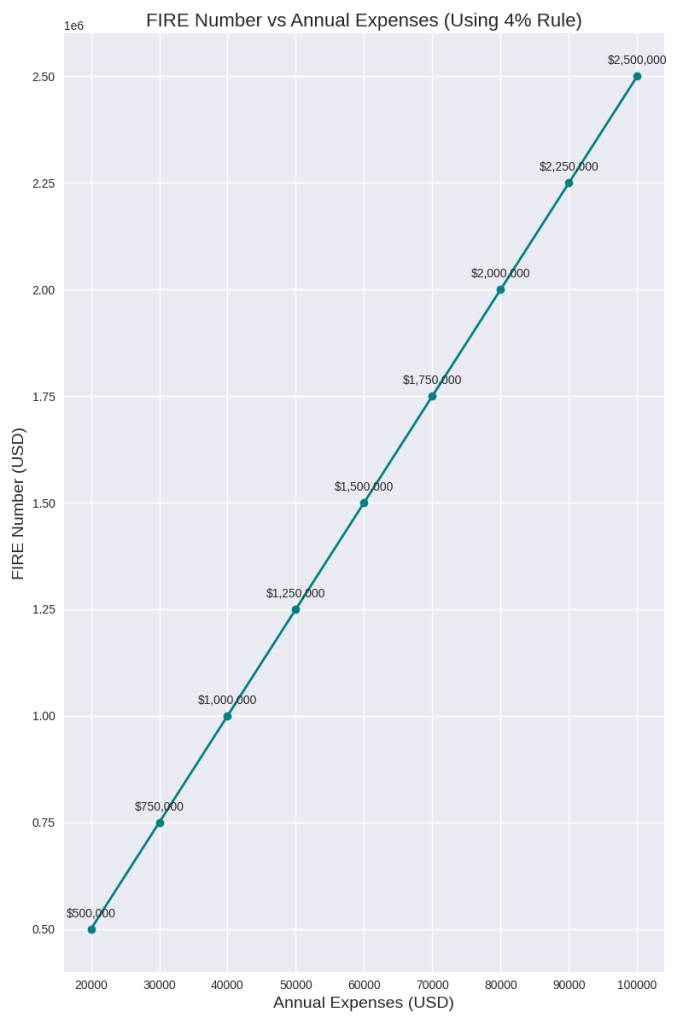

🧮 The Simple Math Formula

Here’s the shortcut FIRE enthusiasts love:

Annual Expenses × 25 = Your FIRE Number

Why 25? Because 1 ÷ 0.04 = 25.

Examples:

- Spend $40,000/year → $40,000 × 25 = $1,000,000 needed.

- Spend $25,000/year → $25,000 × 25 = $625,000 needed.

⚖️ The Caveats

Of course, no rule is perfect. A few things to keep in mind:

- Market fluctuations: The 4% Rule is based on historical data. Future returns may differ.

- Inflation: Your expenses will rise over time, so your withdrawals need to adjust.

- Flexibility matters: If markets dip, spending less for a while can keep your plan on track.

- Longevity: If you retire very early (say in your 30s), you may want to be more conservative (3.5% or even 3%).

🌱 Why It Matters

The beauty of the 4% Rule is that it turns a vague dream (“someday I’ll retire”) into a concrete target. Instead of thinking in terms of income, you start thinking in terms of expenses and savings rate.

For me, it was empowering: suddenly, I could calculate my “FIRE number” and see the path ahead. It made financial independence feel less like a fantasy and more like a math problem I could actually solve.

✨ Closing Thought

The 4% Rule isn’t a guarantee—it’s a guideline. But it’s one of the simplest, most powerful tools for anyone chasing financial independence.

So, what’s your FIRE number? Take your annual expenses, multiply by 25, and you’ll have a starting point. The math is simple—the journey is the exciting part.

Leave a reply to Geoarbitrage 101: Living Well for Less Around the World – VD Cancel reply