🔥 Introduction: Forecasting Freedom

Most people know their next vacation date.

Few know their FIRE date — the day work becomes optional.

Financial Independence, Retire Early (FIRE) isn’t about quitting your job tomorrow. It’s about knowing when you could — and that clarity changes everything.

When you have a timeline for freedom, your decisions become sharper. You spend with purpose, save with conviction, and plan with peace of mind.

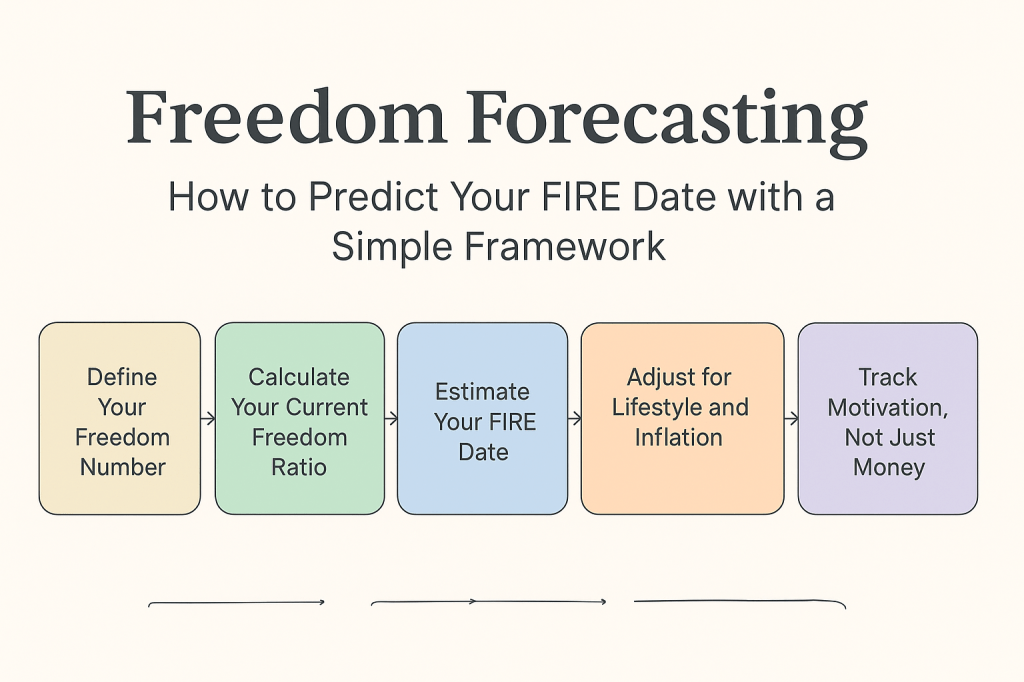

This post introduces a simple system I call Freedom Forecasting — a clear, reality-based framework for predicting your FIRE date, even if you’re early on the journey.

🧭 What Is Freedom Forecasting?

Freedom Forecasting is the practice of projecting when you’ll reach financial independence using your real numbers — not someone else’s spreadsheet.

It’s not about precision; it’s about perspective.

Think of it like checking the weather. You can’t control every variable, but knowing what’s ahead helps you prepare, adjust, and stay the course.

The key idea: your FIRE date = the point where your investments can sustainably fund your life without needing new income.

The math isn’t complicated — but the clarity it brings is life-changing.

💡 Step 1: Define Your “Freedom Number”

Most people start their FIRE journey by guessing: “I think I’ll need a million dollars.”

But FIRE isn’t a fixed number; it’s a personal equation.

Your target depends on your annual spending — not your income, not your age, not your neighbor’s net worth.

Use this simple formula:

Freedom Number = Annual Spending × 25

This is based on the 4% Rule, which suggests you can safely withdraw 4% of your portfolio each year in retirement.

🧮 Example:

If your lifestyle costs $40,000 per year, your Freedom Number is $1,000,000.

That’s the amount where your investments could (theoretically) cover your living costs indefinitely.

Related reading: FIRE Math Made Simple: Breaking Down the 4% Rule

📊 Step 2: Calculate Your Current Freedom Ratio

Once you know your target, figure out how close you are.

Freedom Ratio = (Current Investments ÷ Freedom Number) × 100

If you’ve saved $250,000 toward your $1,000,000 goal, your Freedom Ratio is 25%.

This number tells you how much of your lifestyle is already funded by your assets.

It’s like watching your financial independence “progress bar” fill up — and that’s incredibly motivating.

🕒 Step 3: Estimate Your FIRE Date

Now for the forecasting part.

To estimate your FIRE date, you’ll use three simple variables:

- Current Portfolio – how much you’ve invested

- Annual Contributions – how much you add each year

- Expected Growth Rate – a conservative average (I recommend 5–7%)

With these, you can project when your portfolio will reach your Freedom Number.

You can use any compound growth calculator online, but here’s the basic idea:

Your portfolio grows both from your savings and from compounding returns.

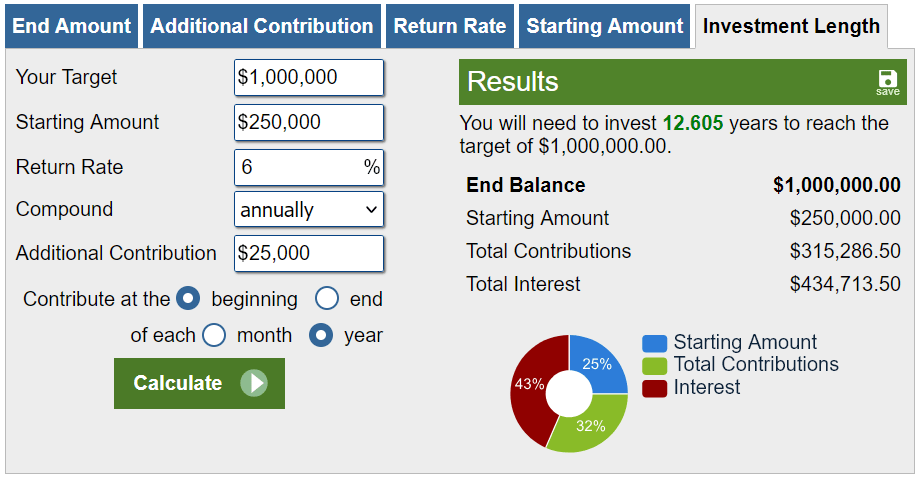

Let’s illustrate:

- Current investments: $250,000

- Annual savings: $25,000

- Growth rate: 6%

- Target: $1,000,000

➡️ Result: You’d likely reach FIRE in about 12 years.

That’s your forecasted freedom date — not a promise, but a powerful direction.

🔄 Step 4: Adjust for Lifestyle and Inflation

Freedom Forecasting isn’t static. Life changes — incomes rise, priorities shift, inflation happens.

Every 6–12 months, revisit your numbers:

- Has your spending changed?

- Are you saving more or less?

- Did market returns outperform or lag expectations?

Recalculate your FIRE date accordingly.

Just like a GPS updates your ETA as you move, your forecast adapts.

That’s the beauty of this system — it keeps you grounded in your real trajectory.

🧘♀️ Step 5: Remember the “FIRE” in FIRE Isn’t Just Money

Forecasting freedom isn’t only about net worth — it’s about life worth.

Knowing your FIRE date helps you design your life before you get there:

- Maybe you hit Coast FIRE — where your investments grow enough on their own — and shift to work you love.

- Maybe you reach Barista FIRE — covering part of your costs through part-time passion projects.

- Or maybe you realize that full retirement isn’t even your goal; freedom is.

Your FIRE date is just a milestone.

What you do with that freedom — how you spend your time, energy, and attention — is the real destination.

💬 Step 6: Track Motivation, Not Just Money

Freedom Forecasting works best when paired with meaning.

You’re not saving for spreadsheets; you’re saving for choices.

Each percentage of your Freedom Ratio represents:

- More creative control.

- More time for family, travel, and health.

- Less dependence on work that drains you.

When you tie your financial metrics to life outcomes, the journey becomes joyful, not just dutiful.

Try this habit:

Each month, note one non-financial win your progress enabled — more time reading, fewer overtime hours, a new skill learned.

That’s your Return on Freedom.

📈 Step 7: Forecast in Layers

Don’t think of FIRE as an all-or-nothing finish line.

Instead, forecast in layers of freedom:

- Mini-FIRE: 1–2 years of expenses saved — short sabbaticals become possible.

- Coast FIRE: You could stop saving and still retire on schedule.

- Lean FIRE: Basic lifestyle covered.

- Fat FIRE: Full lifestyle flexibility.

This layered view keeps you motivated and celebrates progress long before full independence.

🌤️ The Power of Predicting Your FIRE Date

When you know your Freedom Forecast, something shifts.

You move from uncertainty to agency.

From “I hope I can retire someday” to “I’m 38% of the way there.”

It doesn’t matter whether your FIRE date is in 5 years or 15.

The act of forecasting it gives you control, and that’s the foundation of freedom.

💬 Closing Thought

Freedom Forecasting isn’t about guessing the future — it’s about designing it.

It’s a living, breathing framework for turning your financial dreams into timelines and your timelines into plans.

Even if the market wobbles or life reroutes you, you’ll always know where you stand — and that confidence is worth as much as any portfolio gain.

So grab your numbers, open your notebook, and run your first forecast.

Because the moment you can see your FIRE date, you’re already halfway free.

Leave a reply to Halfway to FIRE: Why the First 50% Is Harder Than the Second – VD Cancel reply