If you’re pursuing Financial Independence, you’ve probably spent years optimizing your savings rate, investments, and withdrawal strategy. But here’s the uncomfortable truth most people discover too late: a traditional FIRE (Financial Independence, Retire Early) plan is more fragile than it looks.

Market crashes, inflation spikes, sequence of returns risk, and unexpected life events can quickly threaten even well-funded retirements. The good news? There’s a straightforward way to make FIRE bulletproof that most people completely overlook: the 3-bucket system.

This practical FIRE bucket strategy divides your portfolio based on when you’ll need the money, dramatically reducing risk while increasing peace of mind and flexibility. In this guide, I’ll show you exactly how to build a bulletproof FIRE plan using the 3-bucket system, why it works better than a single-portfolio approach, and how to implement it step by step.

Why Most Traditional FIRE Plans Are Fragile

The classic FIRE approach — save aggressively, invest heavily in stocks, and withdraw 4% annually — works well in theory. In practice, it often fails to account for real-world volatility.

Sequence of returns risk is the biggest threat. If a market downturn hits in the first few years of retirement, you could be forced to sell investments at a loss, permanently shrinking your nest egg. Other hidden risks include longer lifespans, rising healthcare costs, inflation surprises, and large one-time expenses.

During the 2022 bear market, many early retirees watched their safe withdrawal rate suddenly look unsustainable. Those using a single all-stock or balanced portfolio experienced significant stress. A well-designed 3-bucket FIRE system would have protected their near-term spending and given them time to weather the storm.

This is why building a bulletproof FIRE plan requires more than just a high savings rate — it requires intelligent cash flow structuring.

What Is the 3-Bucket System for FIRE?

The 3-bucket system is a simple yet powerful portfolio allocation strategy that separates your money into three distinct “buckets” based on time horizon and risk tolerance:

- Bucket 1: Safety Bucket (Short-term needs)

- Bucket 2: Stability Bucket (Medium-term needs)

- Bucket 3: Growth Bucket (Long-term growth)

Instead of treating your entire portfolio the same, this FIRE bucket strategy matches each portion of money to its specific purpose, creating natural protection against market volatility.

Breaking Down the 3 Buckets in Detail

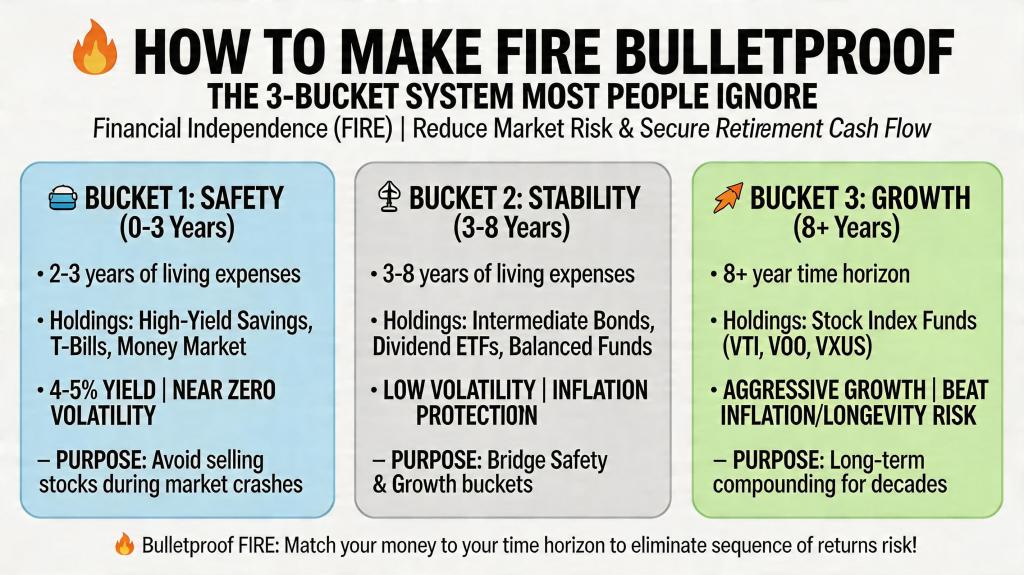

Bucket 1: The Safety Bucket (0–3 Years)

This bucket holds 2–3 years of annual living expenses in ultra-safe, liquid assets. It acts as your emergency and daily spending fund during retirement.

Recommended holdings: High-yield savings accounts, money market funds, short-term Treasury bills, and cash equivalents.

Current expected yield (2026): 4–5% with almost zero volatility.

Purpose: Protect you from having to sell stocks during a crash. This bucket is the foundation of a bulletproof FIRE plan.

Bucket 2: The Stability Bucket (3–8 Years)

This bucket covers medium-term expenses and serves as a bridge between safety and growth. It balances moderate growth with capital preservation.

Recommended holdings: Intermediate-term bonds, bond ladders, conservative balanced funds, and high-quality dividend ETFs.

Expected behavior: Lower volatility than stocks with better inflation protection than cash.

Purpose: Provide reliable income while giving your Growth Bucket time to recover from downturns.

Bucket 3: The Growth Bucket (8+ Years)

This is your long-term compounding engine. Because you won’t touch it for many years, it can stay aggressively invested for maximum growth.

Recommended holdings: Broad stock market index funds (VTI, VOO, VXUS), growth ETFs, and a small allocation to alternatives if desired.

Purpose: Combat longevity risk and inflation over decades.

How to Build and Allocate Your 3-Bucket System

Here’s a practical step-by-step guide to implementing this bulletproof FIRE strategy:

- Determine Your Real Annual Spending

Calculate your true post-FIRE lifestyle number, including healthcare, travel, taxes, and buffer for unexpected costs. - Size Each Bucket

- Safety Bucket: 2–3 years of spending

- Stability Bucket: 4–5 years of spending

- Growth Bucket: Everything remaining (typically 60–75% of your total portfolio)

- Example Allocation

For someone with $60,000 annual spending and a $1.2M portfolio:

- Safety Bucket: $150,000 (2.5 years)

- Stability Bucket: $300,000 (5 years)

- Growth Bucket: $750,000 (62.5%)

- Choose the Right Accounts

Place Safety and Stability buckets in tax-advantaged accounts where possible to minimize taxes on withdrawals. - Create Replenishment Rules

Define clear triggers for moving money between buckets. Example:

- Refill Safety Bucket from Stability Bucket when it falls below 1.5 years.

- Refill Stability Bucket from Growth Bucket only during strong market years (e.g., when S&P 500 is up >15%).

How to Maintain the System Over Time

A bulletproof FIRE plan isn’t set-it-and-forget-it. Review your buckets annually or after major market moves. Rebalance during favorable conditions to lock in gains from the Growth Bucket.

Adjust bucket sizes every 3–5 years as your risk tolerance and life circumstances change. Someone in their early 50s might keep larger Safety and Stability buckets than someone in their late 60s.

Key Advantages of the 3-Bucket FIRE Strategy

- Significantly lower sequence of returns risk

- Greater emotional resilience during market crashes

- Built-in flexibility for big life expenses or opportunities

- Improved longevity protection through sustained growth

- Higher probability of success over 40+ year retirements

Most importantly, it allows you to enjoy Financial Independence without constantly worrying about your portfolio balance.

Common Mistakes to Avoid

- Making the Safety Bucket too small (less than 2 years)

- Being overly conservative across all buckets

- Failing to establish clear replenishment rules

- Ignoring taxes and withdrawal sequencing

- Neglecting to adjust for inflation annually

Real-World Performance

During the 2022 market decline, investors using a 3-bucket system were able to spend from their Safety Bucket without selling stocks at depressed prices. Many reported significantly less stress and better long-term outcomes compared to those using a single-portfolio approach.

Final Thoughts: Building a Truly Bulletproof FIRE Plan

Making FIRE bulletproof isn’t about predicting the future or chasing the highest possible returns. It’s about designing a resilient system that can handle whatever the market and life throw at you.

The 3-bucket system offers a simple, proven framework that most people in the FIRE community still ignore. By separating your money by time horizon, you reduce risk, increase flexibility, and gain the peace of mind that true financial independence should provide.

If you’re approaching FIRE or already there, take time this week to evaluate your current portfolio through the 3-bucket lens. This one change could be the highest-leverage upgrade you make to your entire financial plan.

Your future self — and your portfolio — will thank you.

Related Reading

If you enjoyed this article, these pieces explore more sustainable approaches to Financial Independence:

- Dynamic Withdrawal Rates for FIRE: Why Spending More Early Might Be Safer Than the 4% Rule

- Designing Cash Flow for Financial Independence (Not Maximum Returns)

- Why FIRE Isn’t Sustainable Without Financial Slack

- The Boring Middle of FIRE: How to Stay Consistent While Compounding Works

- Barista FIRE vs. Lean FIRE vs. Fat FIRE Explained

- The 80/20 of FIRE: Tiny Financial Tweaks That Create Outsized Results

- The Optionality Playbook: Why Financial Independence Is About Better Choices

- FIRE Mistakes That Delay Financial Independence (And How to Avoid Them)

Leave a comment