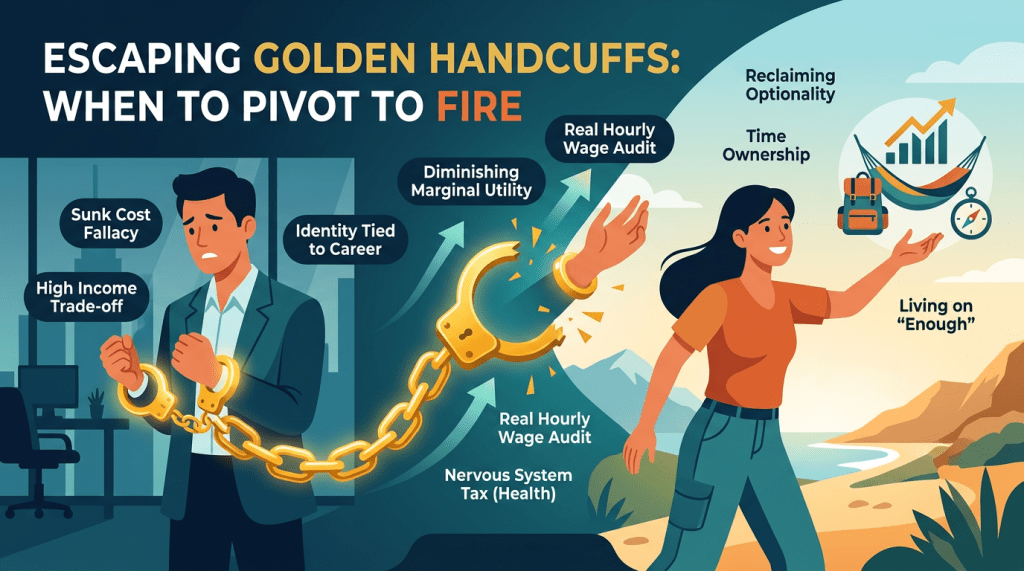

It is a peculiar modern paradox: some of the most “successful” people in the world are also the most trapped.

You see it in the high-rise offices of Manhattan, the tech campuses of Palo Alto, and increasingly, in the Slack channels of high-level remote developers. It’s the phenomenon of the Golden Handcuffs. You’ve reached a level of income that most people only dream of. You have the title, the bonus structure, and the equity. But you also have a mounting sense of dread every time your calendar pings.

You want to pivot towards FIRE (Financial Independence, Retire Early). You’ve run the numbers, and you realize you could probably walk away today and live a meaningful, modest life. Yet, you don’t. You stay. You tell yourself it’s about “security” or “maximizing the opportunity”, but if you look closer, it’s actually a classic cognitive error: The Sunk Cost Fallacy.

In this guide, we are going to deconstruct the psychology of the Golden Handcuffs, analyze the real math behind the high-income trade-off, and provide a framework for knowing exactly when to pivot from “Accumulation” to “Freedom”.

1. The Sunk Cost Fallacy of Your Career

The Sunk Cost Fallacy is the tendency to follow through on an endeavor if we have already invested time, effort, or money into it, whether or not the current costs outweigh the benefits.

In a high-paying career, the “sunk costs” are immense. You didn’t just stumble into your salary. You spent:

- 4–8 years in higher education (and perhaps a mountain of debt).

- A decade or more of 60-hour weeks “paying your dues.”

- Thousands of hours building a specific, niche reputation.

When you look at your life through this lens, quitting feels like “wasting” your 20s and 30s. You feel that because you worked so hard to get the high-paying job, you are obligated to keep the high-paying job.

The Reality Check: Your past effort is gone. It is a “sunk” investment. The only question that matters for your future is: Is the next hour of your life worth the price the market is paying for it?

If you are already 50% or 75% of the way to FIRE, the answer to that question changes drastically. The first $100k you earned bought you survival. The next $100k you earn at the peak of your career might only be buying you a slightly nicer car or a slightly more expensive wine – at the cost of your health, your hobbies, and your youth.

2. The Diminishing Marginal Utility of the Next Dollar

In economics, the law of diminishing marginal utility states that as a person consumes more of a good, the added satisfaction from each additional unit decreases.

Money is no different.

- For someone with $0 net worth: $10,000 is life-changing. It’s security. It’s food. It’s a literal nervous system upgrade.

- For someone with $1.5M net worth: $10,000 is a 0.6% fluctuation in their portfolio. It has almost zero impact on their day-to-day happiness or long-term safety.

When you are wearing Golden Handcuffs, you are often trading your limited, non-renewable time for dollars that have very low marginal utility. You are selling “Life Credits” for “Luxury Credits”.

If your “Enough” number is $1.2 million, and you are currently at $1 million, that final $200k might feel essential. But if your career is so stressful that it is damaging your longevity, that $200k is the most expensive money you will ever earn. You are literally trading years off the end of your life to add digits to a spreadsheet that already covers your needs.

3. The “Real” Hourly Wage Calculation

To escape the Golden Handcuffs, you must stop looking at your gross salary and start looking at your Real Hourly Wage.

A $250,000 salary sounds incredible until you perform a “Lifestyle Beta” audit. To earn that money, what are the hidden costs?

- The Time Cost: Not just the 40 hours in the contract, but the 10 hours of “thinking about work,” the 5 hours of “venting about work,” and the 5 hours of “recovering from work” on the weekend.

- The Health Cost: The gym memberships you pay for but don’t use. The expensive “convenience” food because you’re too tired to cook. The therapy or medication required to manage the stress of being “on” all day.

- The Taxes: High earners in many jurisdictions are taxed at the highest marginal rate. You are working the hardest for the dollars that the government takes the most of.

When you divide your net gain (after taxes and work-related expenses) by your actual time spent (including commute and mental overhead), your $150/hour job often starts looking more like a $40/hour job. Once you see that number, the Golden Handcuffs start to feel a lot more like regular, rusty ones.

4. The Nervous System Tax

Health is the ultimate currency.

High-pressure careers often keep the body in a state of chronic sympathetic (fight-or-flight) activation. This is the “Nervous System Tax”. Over a decade, this tax manifests as:

- Lowered VO2 Max (due to lack of consistent, high-quality training).

- Poor sleep architecture (due to blue light and late-night cortisol spikes).

- Reduced “Idea Carrying Capacity” (due to cognitive burnout).

If you stay in a high-paying job for “just five more years” but those five years move you from “healthy” to “chronically inflamed,” you haven’t won. You’ve just performed a bad trade. You’ve traded your biological capital for financial capital.

You can always earn more money later (via Barista FIRE or consulting), but you cannot “buy back” the mitochondrial health or the joint mobility you lost by sitting in a chair under fluorescent lights for an extra half-decade.

5. How to Pivot: The Exit Strategy

If you suspect you are suffering from the Sunk Cost Fallacy of a high-paying career, here is the system to help you pivot:

Phase 1: Identity Liquidation

Most of the “weight” of the Golden Handcuffs is identity-based. You are “The Senior Architect” or “The VP of Sales”.

- The Fix: Start building an “Identity Portfolio” outside of work. Focus on your reading habits, your travel goals, or your fitness milestones. When your work is no longer the most interesting thing about you, the prospect of quitting becomes much less terrifying.

Phase 2: Lifestyle Prototyping

Don’t quit and go to zero. Instead, test the “Lifestyle Beta”.

- Take a one-month sabbatical or a “Digital Sabbatical.”

- Live on your projected FIRE budget for 90 days while still earning your high salary.

- If you find that your happiness doesn’t drop when your spending drops, the handcuffs have already been unlocked.

Phase 3: The Downshift (Coast FIRE)

Before you go for full “Fat FIRE,” consider Coast FIRE. Use your reputation and skills to negotiate a lower-stress, part-time version of your current role.

- Ask for a 20% pay cut in exchange for a 3rd day off per week.

- This allows you to keep the “Golden” part of the income while removing the “Handcuffs” part of the schedule.

Conclusion: Reclaiming the Lead Role

The most dangerous part of the Golden Handcuffs is that they make you a supporting character in your own life. You become an asset belonging to a corporation, managed by a calendar, and fueled by a paycheck.

The goal of Financial Independence isn’t to sit on a beach and do nothing. The goal is Optionality. It’s the ability to say “No” to a lucrative but soul-crushing opportunity so you can say “Yes” to a book that changes your thinking, a trip that expands your perspective, or a workout that adds a year to your life.

If you have enough to live, stop working to buy your life. You’ve already bought it. It’s time to start living it.

Related Reading

- The Psychology of Enough: How to Redefine Wealth Beyond Money

- Life After Financial Independence: How to Navigate the Identity Crisis When Work No Longer Defines You

- Why Financial Independence Is Really About Slack (Not Early Retirement)

- The Second-Order Effects of Frugality: When Saving Money Starts to Cost You

- Coast FIRE Explained: The Ultimate Lifestyle Upgrade for People Who Don’t Hate Their Jobs

- Time vs Money: Which One Compounds Faster for Long-Term Freedom?

- How to Reduce Financial Stress Without Earning More (The Lifestyle Beta Approach)

- The Boring Middle of FIRE: How to Stay Consistent While Compounding Works

Leave a comment