The number most FIRE (Financial Independence, Retire Early) planners obsess over is their portfolio size. The number that actually determines whether they sleep at night is something far simpler — and far more overlooked.

You’ve done the math.

You know your FI number. You know your safe withdrawal rate. You’ve run the Monte Carlo simulations. You’ve stress-tested your portfolio against historical downturns. You feel ready.

Then the market drops 30% in your first year of early retirement.

Suddenly, the spreadsheet feels very different from real life. You’re watching your portfolio shrink while your expenses stay stubbornly fixed. You know intellectually that sequence of return risk is manageable — but emotionally, every withdrawal feels like you’re sawing off the branch you’re sitting on.

This is where most FIRE plans quietly break down. Not because the math was wrong. Because the cash buffer was either missing, undersized, or misunderstood.

The cash buffer — the liquid, accessible reserve of spending money sitting outside your investment portfolio — is arguably the most important and least discussed variable in early retirement planning. Get it right, and it becomes a shock absorber that makes your entire plan more resilient. Get it wrong, and you’ll either retire with unnecessary anxiety or delay your retirement by years out of fear you can’t quite name.

This post is about getting it right.

What Is a Cash Buffer (and What It Isn’t)?

Let’s start with clarity, because this concept gets conflated with other things.

A cash buffer in the context of FIRE is not:

- Your regular emergency fund (though it overlaps)

- Your investment portfolio

- A savings account you’re actively building toward FI

- A psychological comfort blanket with no strategic purpose

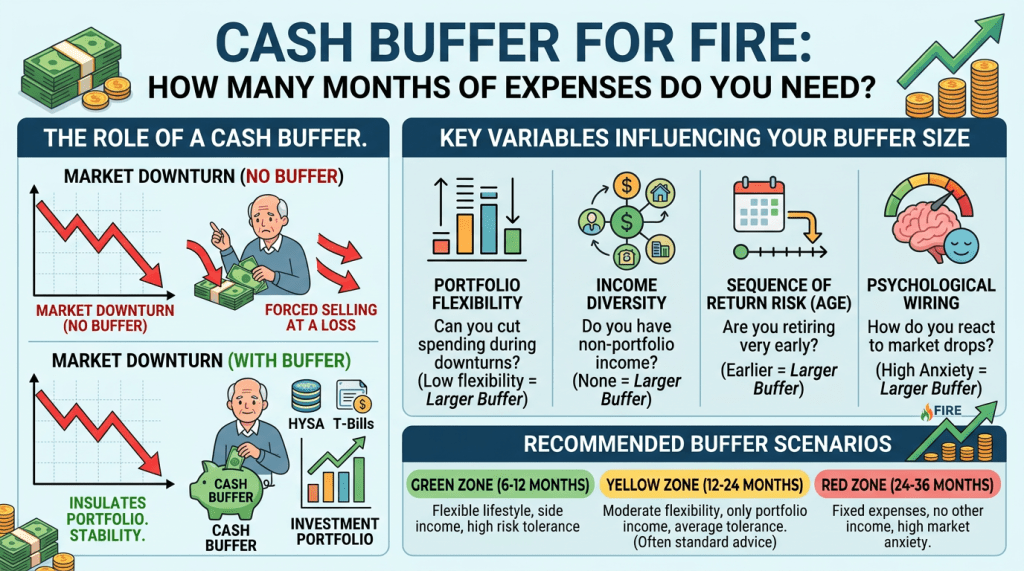

A cash buffer is a dedicated pool of liquid cash — typically held in a high-yield savings account or short-term bonds — that covers a defined number of months of living expenses. Its sole job is to insulate your investment portfolio from forced selling during market downturns.

Here’s why that matters.

When you’re accumulating wealth, market downturns are actually your friend — you’re buying more shares at lower prices. But the moment you retire and start withdrawing, the dynamic flips completely. A bad sequence of returns in your early retirement years — when your portfolio is largest and your withdrawals are proportionally most damaging — can permanently impair your financial independence.

The cash buffer solves this by giving you an alternative source of spending money when markets are down. Instead of selling equities at a loss to fund your lifestyle, you draw from your cash reserve and let your portfolio recover. You’re not timing the market — you’re simply avoiding forced selling at the worst possible time.

Think of it as the shock absorber between your life and your investments.

The Standard Advice (And Why It Falls Short)

Most personal finance advice defaults to one of two positions:

Position 1: The 3–6 Month Emergency Fund

This is the classic advice for working people. Keep 3–6 months of expenses in cash, invest the rest. It’s sensible for someone with a salary, because income arrives reliably every month regardless of what markets do.

Position 2: “Just Trust the 4% Rule”

Some FIRE purists argue that cash buffers are unnecessary — even counterproductive — because holding too much cash creates a drag on long-term returns. The 4% rule, they argue, already accounts for bad sequence-of-return scenarios.

Both positions miss something important.

The 3–6 month emergency fund is designed for employment interruptions, not multi-year bear markets. And the 4% rule, while mathematically sound over long historical periods, doesn’t protect you from the behavioral risk of panic-selling or the practical risk of needing large, irregular expenses in your early retirement years.

The truth is somewhere more nuanced — and more personal.

The Core Question: How Many Months Do You Actually Need?

Here’s the honest answer: it depends on four key variables.

Variable 1: Your Portfolio Flexibility

How rigid are your monthly expenses?

If you can genuinely cut your spending by 20–30% during a market downturn — by traveling less, eating out less, deferring discretionary purchases — you need a smaller cash buffer. Your lifestyle itself becomes part of the shock absorber.

If your expenses are largely fixed — mortgage, healthcare, family obligations — your buffer needs to be larger, because you can’t easily reduce withdrawals when markets fall.

Low flexibility = larger buffer needed.

High flexibility = smaller buffer is acceptable.

Variable 2: Your Income Diversity

Do you have any income streams beyond your portfolio?

Even small amounts of semi-active income dramatically reduce your dependence on portfolio withdrawals — and therefore your need for a large cash buffer.

If you’re doing Barista FIRE with part-time income, freelance consulting, rental income, or a side project that generates even modest cash flow, that income effectively functions as a buffer extension. You’re not fully dependent on your portfolio for every dollar.

If you have zero income beyond your portfolio, your buffer needs to compensate for that fragility.

Zero alternative income = larger buffer needed.

Some alternative income = buffer can be smaller.

Variable 3: Your Sequence of Return Sensitivity

Early retirees are dramatically more sensitive to sequence of return risk than those retiring at traditional ages.

Why? Two reasons:

First, the earlier you retire, the more years your portfolio needs to sustain you. A bad sequence of returns in year one of a 50-year retirement is far more damaging than in year one of a 20-year retirement.

Second, younger retirees often have larger portfolios in absolute terms — meaning each percentage point of loss represents a larger dollar amount.

If you’re retiring in your 30s or 40s, a larger cash buffer is not paranoia — it’s actuarially sound.

Earlier retirement = larger buffer needed.

Later retirement = standard buffer may suffice.

Variable 4: Your Psychological Wiring

This one rarely appears in FIRE calculators, but it may be the most important variable of all.

How do you respond emotionally to market volatility?

Some people can watch their portfolio drop 40% and feel nothing — they understand markets, they trust the math, and they stay the course. For these people, a smaller buffer is perfectly functional. Excess cash is genuinely a drag on returns.

Others — even intellectually sophisticated ones — find that large paper losses trigger anxiety that disrupts sleep, relationships, and decision-making. For them, a larger cash buffer isn’t irrational. It’s the price of staying invested and not making catastrophic decisions driven by fear.

High volatility anxiety = larger buffer is worth the return drag.

High emotional resilience = lean buffer is efficient.

Be honest with yourself here. There’s no virtue in undersizing your buffer to optimize returns if the result is that you panic-sell at the bottom.

The Cash Buffer Framework: A Practical Guide by Scenario

Here’s how to think about buffer sizing across common FIRE scenarios:

🟢 Scenario 1: Flexible Lifestyle + Some Income + High Resilience

Recommended buffer: 6–12 months of expenses

You can cut spending meaningfully if needed, you have occasional income from consulting or freelance work, and you’ve lived through market drops without losing sleep. Your portfolio and lifestyle flexibility are your primary shock absorbers. A 6–12 month buffer is sufficient and efficient.

🟡 Scenario 2: Moderate Flexibility + Portfolio-Only Income + Moderate Resilience

Recommended buffer: 12–24 months of expenses

This is the most common FIRE profile. You’ve optimized your expenses but can’t dramatically reduce them. Your portfolio is your only income source. You understand market volatility intellectually but still feel it emotionally. A 12–24 month buffer gives you enough runway to weather most downturns without forced selling or lifestyle panic.

This is also the buffer size most consistent with historical research on reducing sequence of return risk without excessively dragging long-term returns.

🔴 Scenario 3: Fixed Expenses + Portfolio-Only Income + High Anxiety

Recommended buffer: 24–36 months of expenses

Your expenses are largely non-negotiable — healthcare costs, family obligations, mortgage payments. You have no alternative income. And market volatility genuinely disrupts your wellbeing. A 24–36 month buffer gives you a multi-year runway that covers even prolonged bear markets like 2000–2002 or 2007–2009 without touching your investment portfolio.

Yes, holding this much in cash has a real return cost. But the behavioral and practical protection it provides makes the entire plan more sustainable.

🔵 Scenario 4: Geoarbitrage + Low Fixed Expenses + High Flexibility

Recommended buffer: 6–12 months of expenses (at reduced cost basis)

If you’re pursuing geoarbitrage — living in lower-cost countries where your dollars go significantly further — your buffer calculation changes. Your monthly expenses might be $2,000–$3,000 rather than $5,000–$6,000. A 12-month buffer at $2,500/month is $30,000 — a very manageable and efficient reserve that covers significant market disruption.

Geographic flexibility is itself a form of financial resilience.

Where to Keep Your Cash Buffer

This is a question worth answering specifically, because “cash” doesn’t mean hiding money under a mattress.

High-Yield Savings Accounts (HYSAs)

The default for most people. Fully liquid, FDIC insured, and currently paying meaningful interest. The right home for the bulk of your buffer.

Short-Term Treasury Bills (T-Bills)

For larger buffers, T-bills (3–12 month maturities) offer slightly better yields than most HYSAs with essentially the same risk profile. You can ladder maturities to maintain liquidity while optimizing yield.

Money Market Funds

Offered through most brokerages. Liquid, low-risk, and often yielding competitively. Convenient if you want everything in one investment account.

What to Avoid

Don’t keep your buffer in:

- Long-term bonds (interest rate risk)

- Dividend stocks (market risk defeats the purpose)

- Certificates of deposit without early withdrawal options (liquidity risk)

- Your investment portfolio (that’s the problem you’re trying to solve)

The buffer’s job is stability and liquidity, not returns. Optimize for those two qualities, not yield.

The Bucket System Connection

If you’ve read about the three-bucket system for retirement income, the cash buffer is essentially Bucket One.

- Bucket 1 (Cash): 1–3 years of expenses in liquid form. This is your buffer.

- Bucket 2 (Bonds/Conservative): 3–7 years of expenses in lower-volatility assets. Replenishes Bucket 1 during mild downturns.

- Bucket 3 (Equities): Everything else, invested for long-term growth.

The power of this system is that Bucket 1 gives you the time for Bucket 3 to recover without forced selling. A market crash that lasts 18 months feels entirely different when you have 24 months of expenses in cash. You’re not a forced seller. You’re a patient investor waiting for recovery.

Your cash buffer isn’t just a safety net — it’s what makes the entire three-bucket architecture work.

The Hidden Cost of Getting This Wrong (In Both Directions)

Too little buffer:

- Forced selling during downturns at exactly the wrong time

- Behavioral panic that leads to abandoning your strategy

- Early retirement that feels permanently fragile

- Risk of returning to work not by choice but by necessity

Too much buffer:

- Significant long-term return drag (cash underperforms equities by 4–6% annually over long periods)

- Potentially delaying your FI date unnecessarily

- Opportunity cost that compounds against you over decades

- False security that masks actual portfolio problems

The goal is calibration — finding the minimum buffer that gives you genuine resilience without excessive return sacrifice. That number is personal. But the framework above gives you the tools to calculate it honestly.

How to Build Your Buffer Before You Retire

If you’re still in the accumulation phase, here’s a practical approach:

12–18 months before your target retirement date, begin diverting a portion of new savings into your cash buffer rather than your investment portfolio.

Yes, this slightly slows your portfolio growth in the final stretch. But arriving at retirement with both a fully funded portfolio and a fully funded cash buffer is dramatically safer than arriving with a slightly larger portfolio and no buffer at all.

Think of it as runway construction. You don’t take off without one.

The Real Question Behind the Question

Here’s what I’ve observed talking to people at various stages of their FIRE journey:

The cash buffer question is rarely just about cash.

It’s about confidence. It’s about knowing — not just believing — that your plan can withstand reality. It’s about the difference between a retirement that feels fragile and one that feels robust.

The number of months in your buffer isn’t just a financial calculation. It’s the answer to the question: how long can I sustain my life, completely unaffected, if everything goes wrong at once?

When that answer is 12 months, you feel cautious.

When it’s 24 months, you feel stable.

When it’s 36 months, you feel free.

Financial independence was never just about the portfolio number. It was always about the feeling that number is supposed to produce — the feeling that your life is no longer hostage to forces outside your control.

A well-designed cash buffer doesn’t just protect your money.

It protects your peace of mind.

And that, in the end, is what you were saving for all along.

Related Reading

If this post resonated, here are related articles from the archive worth exploring next:

- How to Make FIRE Bulletproof: The 3-Bucket System Most People Ignore

- Dynamic Withdrawal Rates for FIRE: Why Spending More Early Might Be Safer Than the 4% Rule

- Why FIRE Isn’t Sustainable Without Financial Slack

- Designing Cash Flow for Financial Independence (Not Maximum Returns)

- The Second-Order Effects of Frugality: When Saving Money Starts to Cost You

- Barista FIRE vs. Lean FIRE vs. Fat FIRE Explained: How to Choose the Right Path to Financial Independence

- The Boring Middle of FIRE: How to Stay Consistent While Compounding Works

- Geoarbitrage 101: Living Well for Less Around the World

Leave a comment