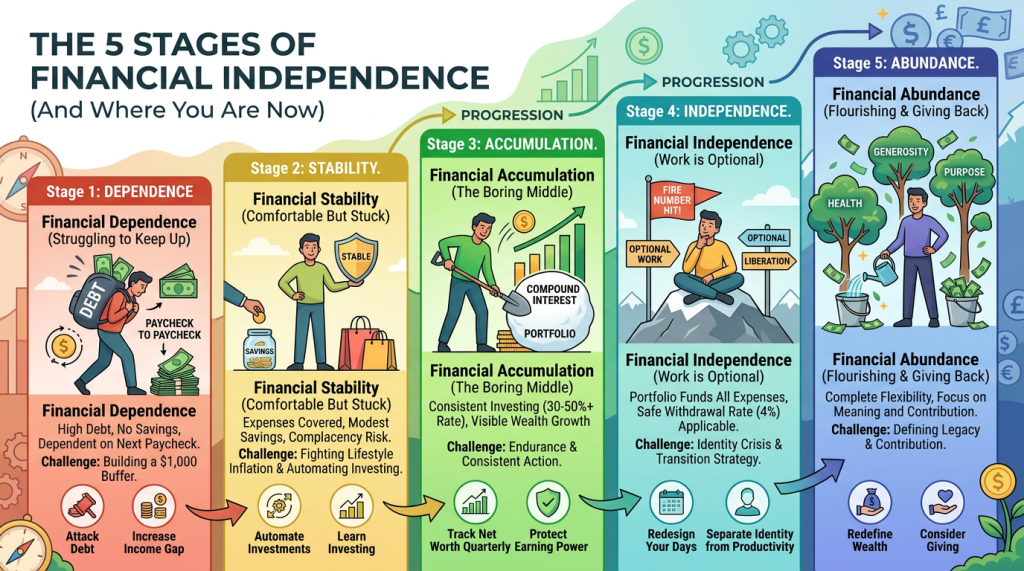

Financial independence isn’t a single destination. It’s a five-stage journey, and most people are stuck at stage two without knowing it. Here’s how to identify where you are and move forward faster.

The Map Most FIRE (Financial Independence, Retire Early) Guides Skip

Most financial independence content focuses on the destination.

Hit your number. Quit your job. Live freely. The end.

But that framing misses something critical. Financial independence isn’t a light switch. It’s not something that happens on a Tuesday when your portfolio crosses a threshold. It’s a journey with distinct phases, each with its own psychology, its own challenges, and its own definition of progress.

The problem is that most people don’t have a map for the journey. They know the destination (freedom) and the vehicle (investing), but they don’t know which stage they’re in, what the terrain of that stage looks like, or how to navigate it without burning out, losing motivation, or making costly mistakes.

That’s what this post is for.

Understanding the five stages of financial independence won’t make the journey shorter. But it will make it clearer. And clarity, in a decade-long pursuit, is worth more than almost any financial optimization.

Let’s start with a question. Of the following five descriptions, which one sounds most like your life right now?

You’re barely keeping up with expenses and debt feels like a ceiling. Or you’re stable but not yet building real wealth. Or you’re investing consistently but the finish line still feels impossibly far. Or your investments could theoretically sustain you, but you’re not ready to stop working. Or you’re living entirely on your own terms, funded by assets, not hours.

One of those hit differently than the others. That’s your stage. Let’s break them all down.

Stage 1: Financial Dependence

What It Looks Like

This is the starting point for almost everyone, though few people recognize it as a stage. At Stage 1, your expenses meet or exceed your income. Debt, whether student loans, credit cards, car payments, or a combination, is a dominant force in your financial life. You are dependent on your next paycheck to cover this month’s bills.

There may be no savings to speak of. An unexpected expense, a broken appliance, a medical bill, a job loss, feels catastrophic because there is no buffer between you and financial crisis.

This stage often carries significant emotional weight. Shame, anxiety, and a sense that everyone else has figured something out that you haven’t. Social media amplifies this. You see people traveling, investing, and talking about retiring at 40 while you’re wondering how to make rent.

Here’s the truth: Stage 1 is not a character flaw. It’s a starting position. Every person who has ever achieved financial independence began here.

The Core Challenge

The psychological challenge at Stage 1 is not financial. It’s motivational. The gap between where you are and where you want to be feels so large that many people give up before they start. Or they never start at all, choosing instead to normalize the situation rather than face it.

The financial challenge is building the first real buffer: an emergency fund. Not investing. Not optimization. Just a small, stable pool of cash that separates you from the next crisis.

How to Navigate It

- Name the number. Calculate your actual monthly expenses with brutal honesty. Most people at Stage 1 don’t know what they spend. Clarity is the first move.

- Build a $1,000 emergency fund before anything else. This single step changes your psychological relationship with money.

- Attack high-interest debt aggressively. Every dollar paid toward a 20% credit card is a guaranteed 20% return. No investment reliably beats that.

- Increase the gap. The only lever that matters at Stage 1 is the difference between income and expenses. Earn more, spend less, or both.

The goal of Stage 1 is not wealth. It’s stability. You’re building the floor.

Stage 2: Financial Stability

What It Looks Like

Stage 2 is where the majority of working adults quietly live their entire financial lives without realizing there’s somewhere further to go.

At Stage 2, you’re not in crisis. Your income covers your expenses with something left over. You might have a small savings account, maybe a retirement fund through your employer, maybe some modest investments. High-interest debt is gone or manageable. You could handle a $2,000 emergency without panic.

From the outside, Stage 2 looks fine. By conventional standards, it is fine. You’re doing better than most. And that’s precisely the danger.

Stage 2 is comfortable enough to stop. The urgency of Stage 1 is gone. You’re no longer in pain. But you haven’t yet built the kind of wealth that creates real freedom. You’re stable, but you’re not free. You’re surviving well, but you’re not compounding.

The Core Challenge

The challenge at Stage 2 is complacency. Lifestyle inflation is the primary enemy here. As income grows, expenses tend to grow with it: a nicer apartment, a newer car, more frequent dining out, a subscription for everything. The gap between income and expenses, the savings rate, stays flat or even shrinks despite a higher salary.

This is the golden handcuff stage. You’re comfortable enough that sacrifice feels unnecessary, but not wealthy enough that work feels optional. Many people spend twenty years here and mistake it for success.

How to Navigate It

- Protect your savings rate, not your lifestyle. Every raise is an opportunity. The question is whether it goes to your savings rate or your spending. Aim to save at least 20% of income. The FIRE community typically targets 40–60%.

- Automate investing. Remove the decision from your monthly routine. Set up automatic transfers to index funds the day after your paycheck arrives. Pay your future self first.

- Learn the language of investing. Index funds, expense ratios, asset allocation, tax-advantaged accounts. This is the stage to build financial literacy, not because you have a lot to invest, but because understanding the system early changes everything.

- Fight lifestyle inflation deliberately. Not by living miserably, but by being intentional. Spend on what genuinely improves your life. Cut ruthlessly on what doesn’t.

The goal of Stage 2 is to build momentum. Stability is not the finish line. It’s the launchpad.

Stage 3: Financial Accumulation

What It Looks Like

Stage 3 is where the FIRE journey truly begins. You have a meaningful investment portfolio. You’re saving and investing consistently, 30, 40, 50% or more of your income. Your net worth is growing in a way that’s visible month to month and dramatic year to year.

You understand compound interest not just intellectually but experientially. You’ve watched your portfolio grow by more in a single year than you earned in your first job. The math has become visceral.

Stage 3 often brings a new kind of energy. There’s a clarity of purpose that comes from tracking progress toward a meaningful goal. Many people describe this as the most motivated they’ve ever felt about money.

But Stage 3 also has a shadow side.

The Core Challenge

The challenge at Stage 3 is endurance. The FIRE journey at this stage is often called “the boring middle,” and for good reason. You know what to do. You’re doing it. But the destination is still years away. The novelty has worn off. Market downturns test your conviction. Life changes, relationships, career shifts, health events, introduce new variables.

This is where many people either abandon the path or, equally dangerous, over-optimize. They obsess over expense ratios, tax strategies, and portfolio allocation to the point of diminishing returns, spending enormous cognitive energy on decisions that move the needle by fractions of a percent while ignoring the bigger levers.

How to Navigate It

- Automate and ignore (mostly). Your primary job at Stage 3 is to keep investing consistently. The strategy is less important than the consistency. A simple three-fund portfolio that you contribute to every month will outperform a complex strategy you second-guess constantly.

- Track net worth quarterly, not daily. Daily portfolio checking at Stage 3 is a psychological hazard. It amplifies volatility and encourages emotional decisions. Quarterly reviews give you enough signal without the noise.

- Protect your earning power. At Stage 3, your income is the fuel. Career growth, skill development, and health are financial assets. A burnout that derails your income for a year costs far more than a bad investment decision.

- Build non-financial resources. Community, purpose, physical health, and identity outside of work. These matter enormously when you arrive at Stage 4 and 5. The people who struggle most in early retirement are those who invested everything in their portfolio and nothing in the rest of their life.

The goal of Stage 3 is to trust the process long enough for compounding to do its job. The most valuable skill here is patience with momentum.

Stage 4: Financial Independence

What It Looks Like

This is the stage that the entire FIRE movement points toward. Your investment portfolio is large enough that, using a safe withdrawal rate (typically 3.5–4%), it can fund your annual expenses indefinitely. You have, by the traditional definition, reached financial independence.

You could stop working today and never need a paycheck again.

And yet, many people arrive here and don’t feel free.

This is one of the most underreported phenomena in the FIRE community. People hit their number and expect a wave of liberation. Instead, they often feel a strange combination of uncertainty, purposelessness, and something that feels unsettlingly like fear.

Why? Because financial independence removes the external structure that most people have organized their entire adult life around. The alarm clock, the schedule, the colleagues, the performance review, the sense of being needed. It’s all optional now. And optional, it turns out, can feel terrifying.

The Core Challenge

The challenge at Stage 4 is identity, not money. The financial question has been answered. The human question, who am I without work defining me? has barely been asked.

There’s also a practical challenge: the transition itself. Should you quit immediately? Go part-time? Start something new? The optionality that FIRE promised can paradoxically create decision paralysis.

How to Navigate It

- Give yourself a transition period. You don’t have to quit the day your portfolio crosses the number. Many people take 6–12 months to test different structures: reduced hours, a sabbatical, a creative project. Use this time to prototype life without work before committing.

- Redesign your days intentionally. Freedom without structure becomes aimlessness. Build new rhythms: morning routines, learning projects, physical practices, creative pursuits. The goal isn’t to fill time but to fill it with things that matter.

- Revisit your withdrawal strategy. The 4% rule is a starting point, not a law. Consider dynamic withdrawal rates that flex with market conditions. Build a cash buffer of 12–24 months of expenses to insulate yourself from sequence-of-returns risk in early retirement.

- Separate identity from productivity. This is the deep work of Stage 4. Your worth as a person is not your output. This sounds obvious. It takes most people years to truly believe it.

The goal of Stage 4 is to learn how to be financially independent, not just be it numerically.

Stage 5: Financial Abundance

What It Looks Like

Stage 5 is beyond the traditional FIRE definition. Here, your portfolio has grown beyond what you need. Your investments generate more than you spend, and the surplus compounds further. You have complete flexibility in how, where, and whether you work.

At Stage 5, money has largely ceased to be a daily variable in your decision-making. You don’t think about whether you can afford something reasonable. You think about whether it aligns with the life you want to live.

More importantly, Stage 5 is characterized by a psychological shift. The anxiety that money carries for most people, even most people at Stage 4, is largely gone. Decisions are made from abundance, not scarcity. Generosity becomes natural. Risk feels different when you have more than enough.

The Core Challenge

The challenge at Stage 5 is meaning and contribution. When your own needs are fully met, the questions that surface are larger: What do I want to create? Who do I want to help? What legacy matters to me?

These aren’t financial questions. They’re existential ones. And many people find that Stage 5 without a clear answer to those questions can feel surprisingly hollow.

How to Navigate It

- Redefine wealth beyond money. The most valuable things at Stage 5 are time, relationships, health, and contribution. Invest in all four deliberately.

- Consider giving as a wealth strategy. Not just charitable giving, but giving of time, mentorship, knowledge, and access. The research on subjective well-being consistently shows that spending on others produces more happiness than spending on yourself beyond a certain income threshold.

- Stay physically and intellectually engaged. The longevity research is clear: purpose, movement, and continued learning are the variables that predict healthy aging. Financial abundance without physical and cognitive investment produces a shorter, less vital life.

- Build a legacy framework. Not necessarily in the traditional estate-planning sense, but in the sense of asking: what do you want to have contributed? To your family, your community, your field?

The goal of Stage 5 is to turn financial freedom into a platform for something larger than yourself.

Where Are You Now?

Read back through the five stages. One of them described your life more accurately than the others. That’s your current stage. Not your permanent address. Your current position on a map.

The map matters because it changes how you make decisions. At Stage 1, the right move is different from Stage 3. At Stage 4, the challenges are different from anything the financial math prepared you for.

Knowing your stage also protects you from comparison. Someone at Stage 3 comparing themselves to someone at Stage 5 is like a runner at mile 8 feeling demoralized by someone at mile 20. You’re on the same course. You’re just at different points.

The work is to navigate your current stage well. Not to skip stages. Not to rush. But to understand the terrain, avoid the specific pitfalls of where you are, and keep moving forward with intention.

Financial independence is a long game. But it’s a game with a map.

Now you have one.

Related Reading

If this post resonated, these earlier posts will take your thinking further:

- The Boring Middle of FIRE: How to Stay Consistent While Compounding Works

- Life After Financial Independence: How to Navigate the Identity Crisis When Work No Longer Defines You

- The Freedom Gap: Why Hitting Your Number Doesn’t Feel Like Freedom

- Why Financial Independence Is Really About Slack (Not Early Retirement)

- Financial Independence is a Skill, Not a Number

- The Psychology of Enough: How to Redefine Wealth Beyond Money

- Halfway to FIRE: Why the First 50% Is Harder Than the Second

- The Optionality Playbook: Why Financial Independence Is About Better Choices, Not Early Retirement

Leave a comment